Market Value (000s)

Duration (Years)

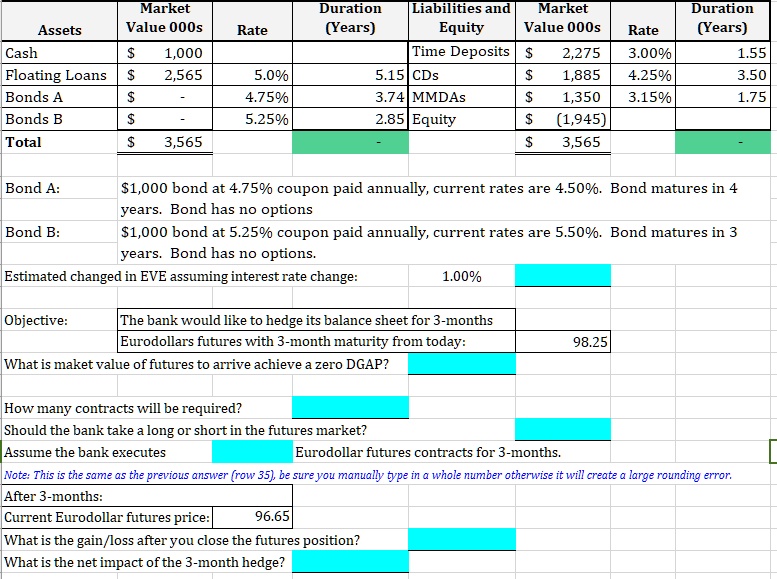

Liabilities and Market Duration

Equity Value (000s)

Rate (Years)

Time Deposits $2,275 3.00% 1.55 5.15

CDs $1,885 4.25% 3.50 3.74

MMDAs $1,350 3.15% 1.75 2.85

Equity $ (1,945) $3,565

Assets

Cash $1,000

Floating Loans $2,565

Bonds A

Bonds B

Total $3,565

Rate

5.0%

4.75%

5.25%

Bond A:

$1,000 bond at 4.75% coupon paid annually, current rates are 4.50%. Bond matures in 4 years. Bond has no options

Bond B:

$1,000 bond at 5.25% coupon paid annually, current rates are 5.50%. Bond matures in 3 years. Bond has no options. Estimated change in EVE assuming interest rate change: 1.00%

Objective:

The bank would like to hedge its balance sheet for 3-months Eurodollars futures with 3-month maturity from today: 98.25

What is the market value of futures to achieve a zero DGAP?

How many contracts will be required?

Should the bank take a long or short position in the futures market?

Assume the bank executes Eurodollar futures contracts for 3 months

Note: This is the same as the previous answer (row 35), be sure you manually type in a whole number otherwise it will create a large rounding error

After 3 months:

Current Eurodollar futures price: 96.65

What is the gain/loss after you close the futures position?

What is the net impact of the 3-month hedge?