XYZ Insurance Co wants to buy a block of structured settlement annuities.

The expected cash flows of the block have been calculated by the actuary of the selling company. They are the following:

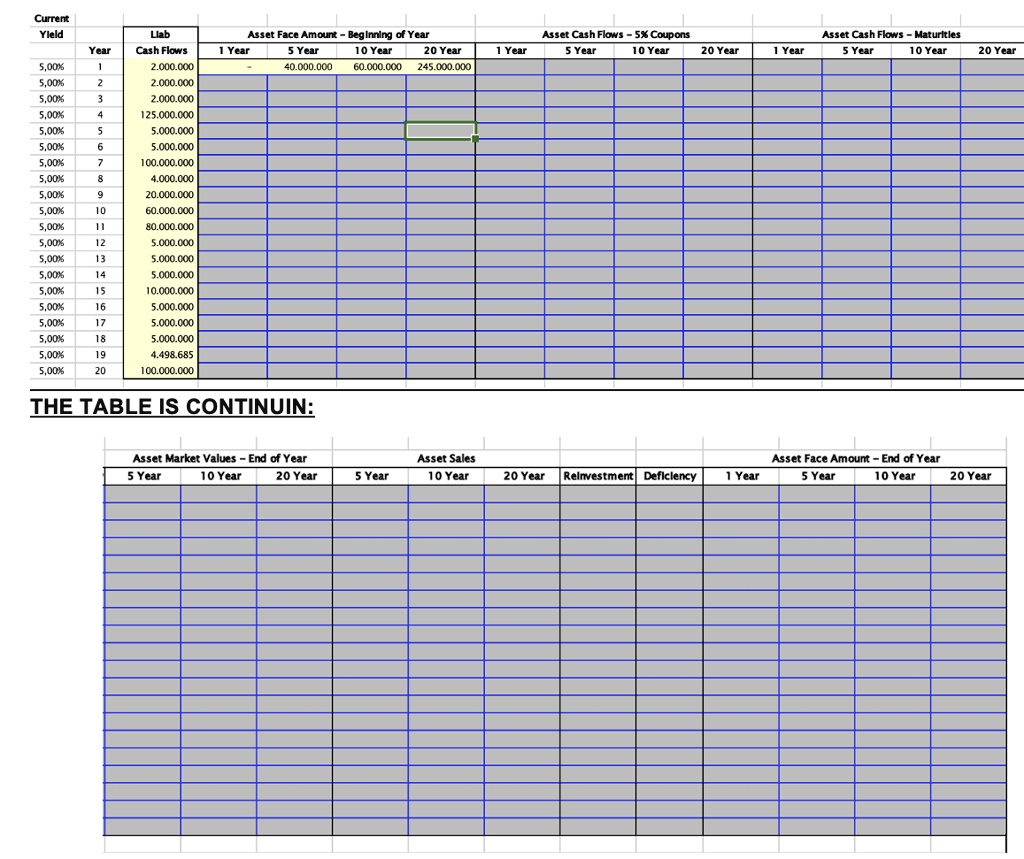

Liab

Year Cash Flows

1 2,000,000

2 2,000,000

3 2,000,000

4 125,000,000

5 5,000,000

6 5,000,000

7 100,000,000

8 4,000,000

9 20,000,000

10 60,000,000

11 80,000,000

12 5,000,000

13 5,000,000

14 5,000,000

15 10,000,000

16 5,000,000

17 5,000,000

18 5,000,000

19 4,498,685

20 100,000,000

This block is supported by a portfolio of three assets:

• 5-Year Bond - 5% coupon - €40,000,000

• 10-Year Bond - 5% coupon - €60,000,000

• 20-Year Bond - 5% coupon - €245,000,000

For this analysis, you will work only with annual cash flows. Therefore, you will assume that the coupons on the bonds are paid annually at the end of the year and also that the liability cash flows occur at the end of the year.

Also, you will assume the market rate on all assets is 5%.

The task in this exercise is to project the net cash flow from the assets and liabilities. At the end of each period, the company has to either fund this cash flow (if it is negative) or reinvest the cash if it is positive. If the cash flow is negative, it will sell assets (shortest assets first) to cover the negative balance. If it is positive, it will reinvest the excess in 1-year bonds paying the current market rate. Remember, when it sells an asset, its market value is the present value of future cash flows discounted at the current market rate. Other points to note:

• The market value of an asset is based on the interest rate in that period.

• The one-year bond gets reinvested at the rate available in the year it is purchased.

• If a portion of an asset is sold, its remaining face will decrease proportionate to the amount of market value sold.

COMPLETE THE FOLLOWING TABLE:

Current Yield

Liab Cash Flows 2,000,000 2,000,000 2,000,000 125,000,000 5,000,000 5,000,000 100,000,000 4,000,000 20,000,000 60,000,000 80,000,000 5,000,000 5,000,000 5,000,000 10,000,000 5,000,000 5,000,000 5,000,000 4,498,685 100,000,000

Asset Face Amount -- Beginning of Year 1 Year 5 Year 10 Year 20 Year - 40,000,000 60,000,000 245,000,000

Asset Cash Flows 5% Coupons 1 Year 5 Year 10 Year 20 Year

Asset Cash Flows - Maturities 5 Year 10 Year

Year 1 2 3

1 Year

20 Year

5.00% 5.00% 5.00% 5.00% 5.00% 5.00% 5.00% 5.00% 5.00% 5.00% 5.00% 5.00% 5.00% 5.00% 5.00% 5.00% 5.00% 5.00% 5.00% 5.00%

5

6

8 9 10 11 12 13 14 15 16 17 18 19 20

THE TABLE IS CONTINUING:

Asset Market Values -- End of Year 5 Year 10 Year 20 Year

Asset Sales 10 Year

Asset Face Amount End of Year 1 Year 5 Year 10 Year 20 Year

5 Year

20 Year

Reinvestment Deficiency