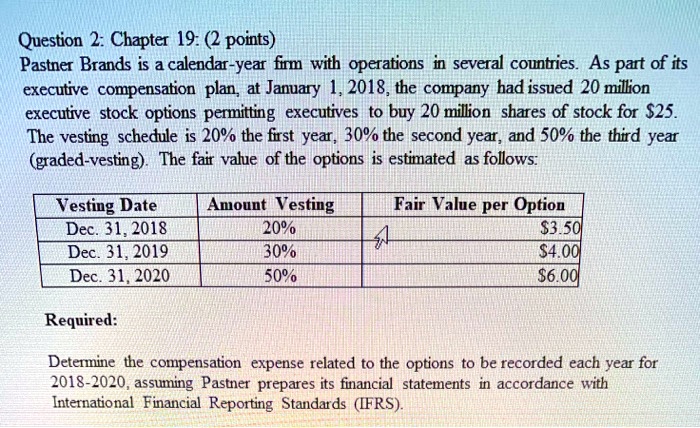

Question 2: Chapter 19: (2 points)

Pastner Brands is a calendar-year firm with operations in several countries. As part of its

executive compensation plan, at January 1, 2018, the company had issued 20 million

executive stock options permitting executives to buy 20 million shares of stock for $25.

The vesting schedule is 20% the first year, 30% the second year, and 50% the third year

(graded-vesting). The fair value of the options is estimated as follows:

Vesting Date Amount Vesting Fair Value per Option

Dec. 31, 2018 20% $3.50

Dec. 31, 2019 30% $4.00

Dec. 31, 2020 50% $6.00

Required:

Determine the compensation expense related to the options to be recorded each year for

2018-2020, assuming Pastner prepares its financial statements in accordance with

International Financial Reporting Standards (IFRS).