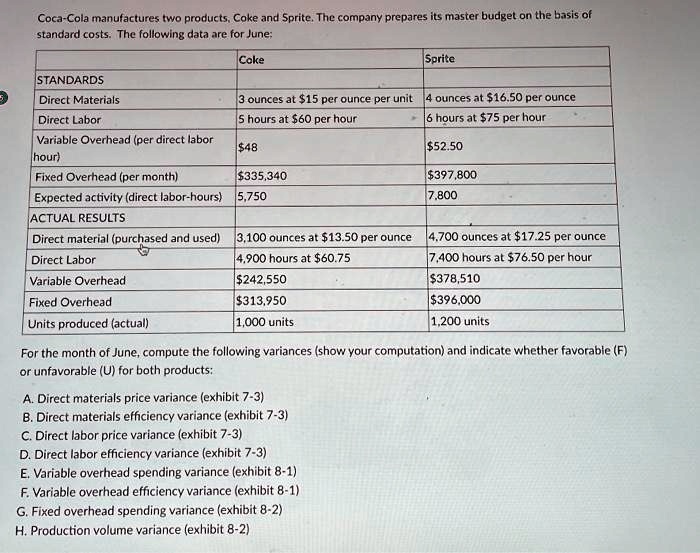

Coca-Cola manufactures two products, Coke and Sprite. The company prepares its master budget on the basis of

standard costs. The following data are for June:

STANDARDS

Direct Materials

Coke

Sprite

3 ounces at $15 per ounce per unit 4 ounces at $16.50 per ounce

Direct Labor

5 hours at $60 per hour

6 hours at $75 per hour

Variable Overhead (per direct labor

$48

$52.50

hour)

Fixed Overhead (per month)

$335,340

$397,800

Expected activity (direct labor-hours) 5,750

7,800

ACTUAL RESULTS

Direct material (purchased and used) 3,100 ounces at $13.50 per ounce 4,700 ounces at $17.25 per ounce

Direct Labor

4,900 hours at $60.75

7,400 hours at $76.50 per hour

Variable Overhead

$242,550

$378,510

Fixed Overhead

$313,950

$396,000

Units produced (actual)

1,000 units

1,200 units

For the month of June, compute the following variances (show your computation) and indicate whether favorable (F)

or unfavorable (U) for both products:

A. Direct materials price variance (exhibit 7-3)

B. Direct materials efficiency variance (exhibit 7-3)

C. Direct labor price variance (exhibit 7-3)

D. Direct labor efficiency variance (exhibit 7-3)

E. Variable overhead spending variance (exhibit 8-1)

F. Variable overhead efficiency variance (exhibit 8-1)

G. Fixed overhead spending variance (exhibit 8-2)

H. Production volume variance (exhibit 8-2)