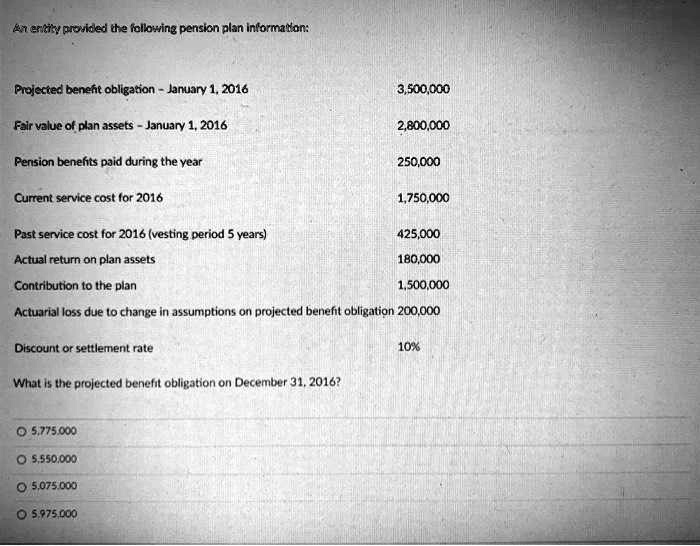

An entity provided the following pension plan information:

Projected benefit obligation - January 1, 2016

3,500,000

Fair value of plan assets - January 1, 2016

2,800,000

Pension benefits paid during the year

250,000

Current service cost for 2016

1,750,000

Past service cost for 2016 (vesting period 5 years)

425,000

Actual return on plan assets

180,000

Contribution to the plan

1,500,000

Actuarial loss due to change in assumptions on projected benefit obligation 200,000

Discount or settlement rate

10%

What is the projected benefit obligation on December 31, 2016?

? 5,775,000

? 5,550,000

? 5,075,000

? 5,975,000