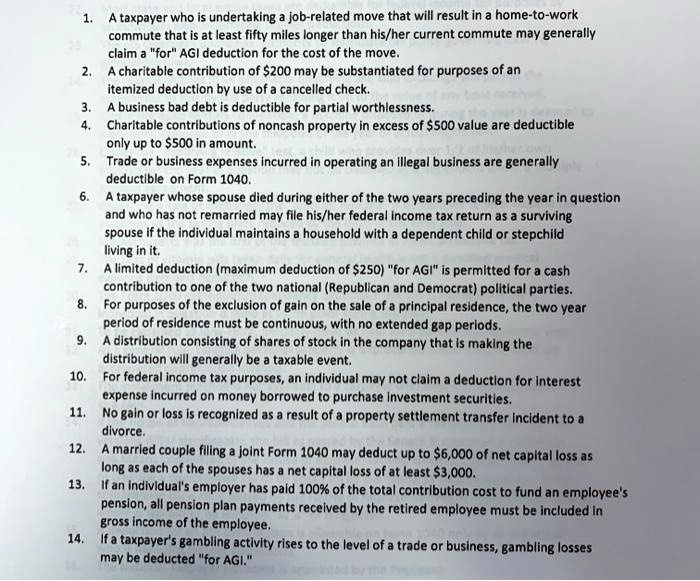

A taxpayer who is undertaking a job-related move that will result in a home-to-work commute that is at least fifty miles longer than his/her current commute may generally claim a "for" AGI deduction for the cost of the move. A charitable contribution of $200 may be substantiated for purposes of an itemized deduction by use of a cancelled check. A business bad debt is deductible for partial worthlessness. Charitable contributions of noncash property in excess of $500 value are deductible only up to $500 in amount. Trade or business expenses incurred in operating an illegal business are generally deductible on Form 1040. A taxpayer whose spouse died during either of the two years preceding the year in question and who has not remarried may file his/her federal income tax return as a surviving spouse if the individual maintains a household with a dependent child or stepchild living in it. A limited deduction (maximum deduction of $250) "for AGI" is permitted for a cash contribution to one of the two national (Republican and Democrat) political parties. For purposes of the exclusion of gain on the sale of a principal residence, the two-year period of residence must be continuous, with no extended gap periods. A distribution consisting of shares of stock in the company that is making the distribution will generally be a taxable event. For federal income tax purposes, an individual may not claim a deduction for interest expense incurred on money borrowed to purchase investment securities. No gain or loss is recognized as a result of a property settlement transfer incident to a divorce. A married couple filing a joint Form 1040 may deduct up to $6,000 of net capital loss as long as each of the spouses has a net capital loss of at least $3,000. If an individual's employer has paid 100% of the total contribution cost to fund an employee's pension, all pension plan payments received by the retired employee must be included in the gross income of the employee. If a taxpayer's gambling activity rises to the level of a trade or business, gambling losses may be deducted "for AGI.