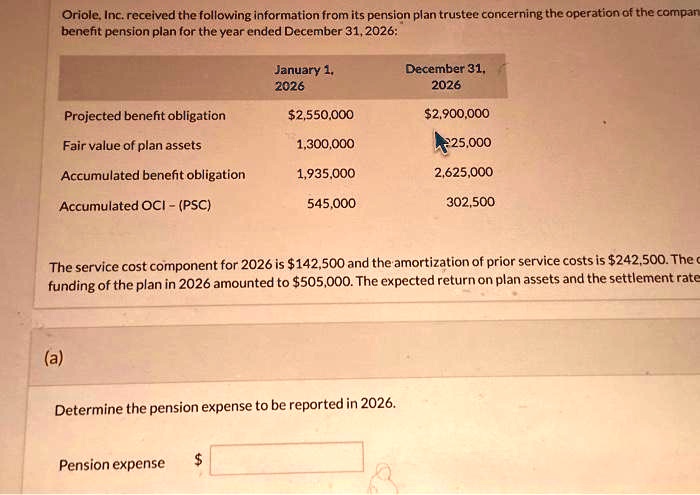

Oriole, Inc. received the following information from its pension plan trustee concerning the operation of the company benefit pension plan for the year ended December 31, 2026:

January 1, 2026 | December 31, 2026

Projected benefit obligation: $2,550,000 | $2,900,000

Fair value of plan assets: 1,300,000 | [partially obscured]

Accumulated benefit obligation: 1,935,000 | 2,625,000

Accumulated OCI - (PSC): 545,000 | 302,500

The service cost component for 2026 is $142,500 and the amortization of prior service costs is $242,500. The funding of the plan in 2026 amounted to $505,000. The expected return on plan assets and the settlement rate

(a)

Determine the pension expense to be reported in 2026.

Pension expense $