Each of the four independent situations below describes a finance lease in which annual lease payments are payable at the beginning of each year. The lessee is aware of the lessor's implicit rate of return.

Note: Use tables, Excel, or a financial calculator. (FV of $1, PV of $1, FVA of $1, PVA of $1, FVAD of $1 and PVAD of $1)

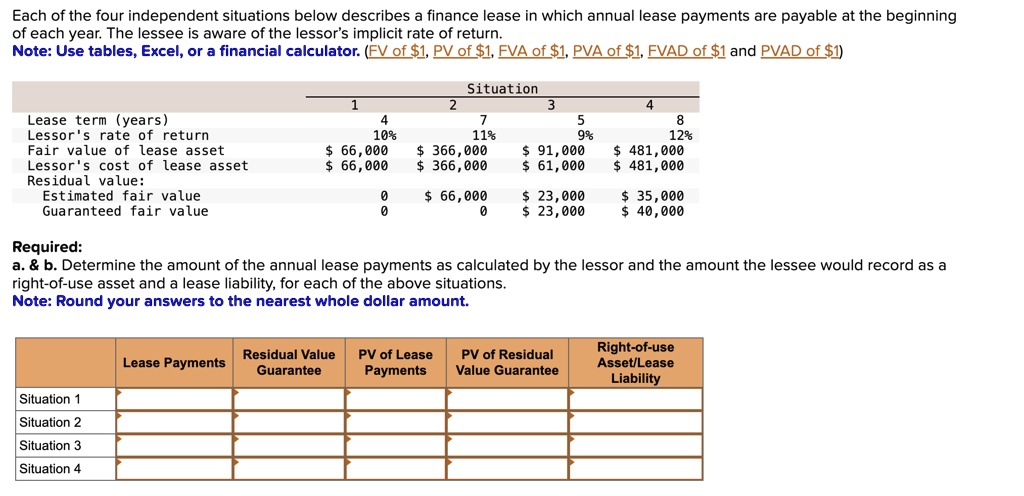

Situation

Lease term (years)

Lessor's rate of return

Fair value of lease asset

Lessor's cost of lease asset

Residual value:

Estimated fair value

Guaranteed fair value

Required:

a. & b. Determine the amount of the annual lease payments as calculated by the lessor and the amount the lessee would record as a right-of-use asset and a lease liability, for each of the above situations.

Note: Round your answers to the nearest whole dollar amount.

Lease Payments

Residual Value

Guarantee

PV of Lease

Payments

PV of Residual

Value Guarantee

Right-of-use

Asset/Lease

Liability

Situation 1

Situation 2

Situation 3

Situation 4

1

4

10%

$ 66,000

$ 66,000

0

0

2

7

11%

$ 366,000

$ 366,000

$ 66,000

0

3

5

9%

$ 91,000

$ 61,000

$ 23,000

$ 23,000

4

8

12%

$ 481,000

$ 481,000

$ 35,000

$ 40,000