You determine the following facts about each of the first five checks: (1) the date of the cash disbursements journal entry is the same as the date of the check, (2) the payee receives the check two days later, (3) the payee records and deposits the check on the day it is received, and (4) it takes five days for a deposited check to clear banking channels and be paid by the bank on which it is drawn. Check 3402 was not recorded as a disbursement until July 1. This check was picked up by the payee on the date it was issued, and it was included in the payee's after-hours bank deposit on June 30.

What are the purposes of the audit of bank transfers?

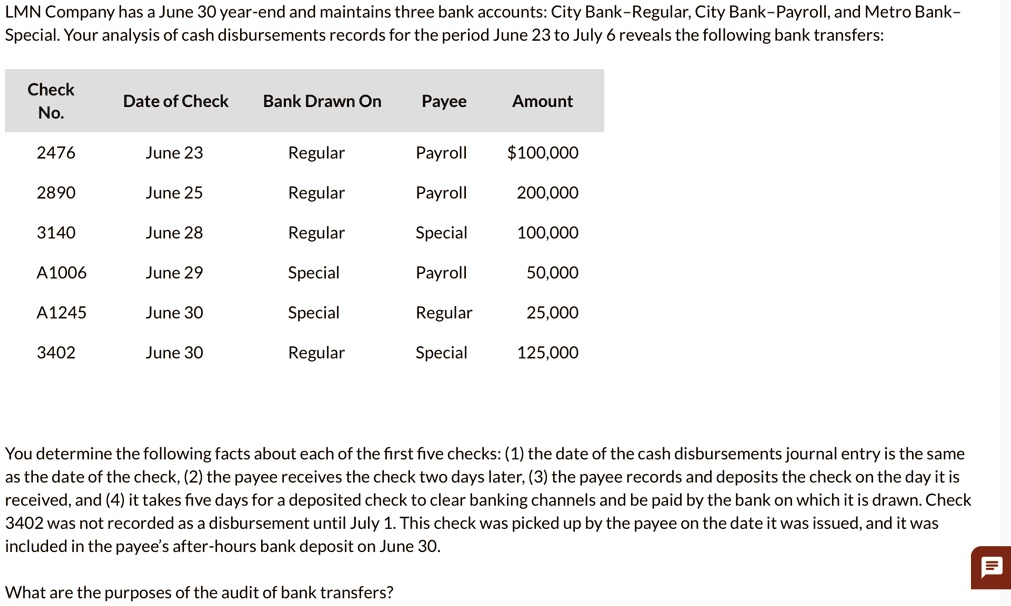

LMN Company has a June 30 year-end and maintains three bank accounts: City Bank-Regular, City Bank-Payroll, and Metro Bank- Special. Your analysis of cash disbursements records for the period June 23 to July 6 reveals the following bank transfers:

Check No.

Date of Check

Bank Drawn On

Payee

Amount

2476

June 23

Regular

Payroll

$100,000

2890

June 25

Regular

Payroll

$200,000

3140

June 28

Regular

Special

$100,000

A1006

June 29

Special

Payroll

$50,000

A1245

June 30

Special

Regular

$25,000

3402

June 30

Regular

Special

$125,000