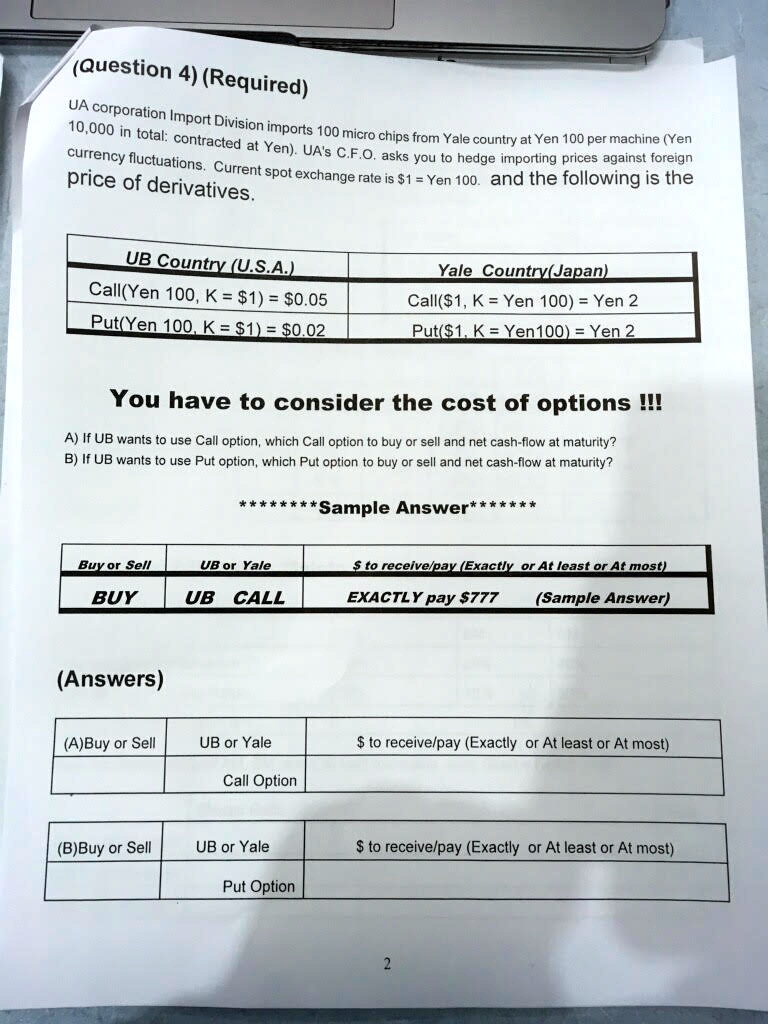

(Question 4) (Required)

UA corporation Import Division imports 100 micro chips from Yale country at Yen 100 per machine (Yen

10,000 in total: contracted at Yen). UA's C.F.O. asks you to hedge importing prices against foreign

currency fluctuations. Current spot exchange rate is $1 = Yen 100. and the following is the

price of derivatives.

UB Country (U.S.A.)

Call(Yen 100, K = $1) = $0.05

Put(Yen 100, K = $1) = $0.02

Yale Country(Japan)

Call($1, K = Yen 100) = Yen 2

Put($1, K= Yen100) = Yen 2

You have to consider the cost of options !!!

A) If UB wants to use Call option, which Call option to buy or sell and net cash-flow at maturity?

B) If UB wants to use Put option, which Put option to buy or sell and net cash-flow at maturity?

********Sample Answer********

Buy or Sell

UB or Yale

$ to receive/pay (Exactly or At least or At most)

BUY

UB CALL

EXACTLY pay $777

(Sample Answer)

(Answers)

(A)Buy or Sell

UB or Yale

$ to receive/pay (Exactly or At least or At most)

Call Option

(B)Buy or Sell

UB or Yale

$ to receive/pay (Exactly or At least or At most)

Put Option

2