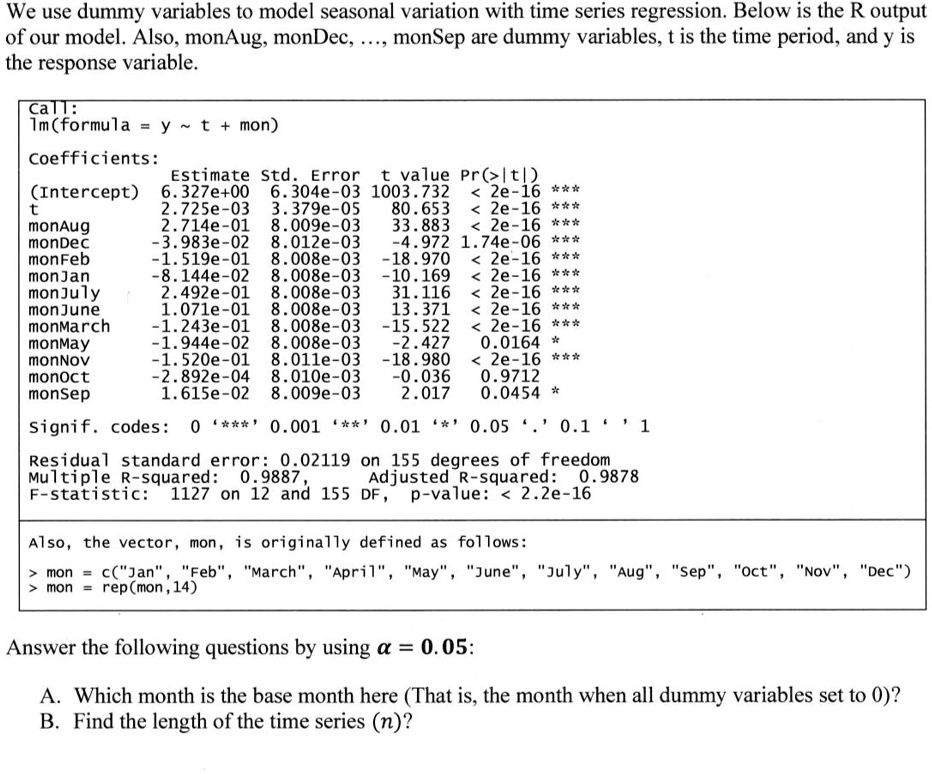

We use dummy variables to model seasonal variation with time series regression. Below is the R output of our model. Also, monAug, monDec,..., monSep are dummy variables, t is the time period, and y is the response variable.

Cal 1mformu1a=y~t+mon

Coefficients:

Estimate Std.Error t value Pr(>ltl

(Intercept) 6.327e+00 6.304e-03 1003.732 <2e-16***

t 2.725e-03 3.379e-05 80.653 <2e-16***

monAug 2.714e-01 8.009e-03 33.883 <2e-16***

monDec -3.983e-02 8.012e-03 -4.972 1.74e-06***

monFeb -1.519e-01 8.008e-03 -18.970 <2e-16***

monJan -8.144e-02 8.008e-03 -10.169 <2e-16***

monJuly 2.492e-01 8.008e-03 31.116 <2e-16***

monJune 1.071e-01 8.008e-03 13.371 <2e-16***

monMarch -1.243e-01 8.008e-03 -15.522 <2e-16***

monMay -1.944e-02 8.008e-03 -2.427 0.0164

monNov -1.520e-01 8.011e-03 -18.980 <2e-16***

monoct -2.892e-04 8.010e-03 -0.036 0.9712

monSep 1.615e-02 8.009e-03 2.017 0.0454

Signif.codes: 0*** 0.001** 0.01* 0.05. 0.11

Residual standard error: 0.02119 on 155 degrees of freedom

Multiple R-squared: 0.9887, Adjusted R-squared: 0.9878

F-statistic: 1127 on 12 and 155 DF, p-value: < 2.2e-16

Also, the vector, mon, is originally defined as follows:

aa.oN..so.os...bnv...nc..ounc.ew..uav...yuew.qo..uec..=uo mon=rep(mon,14)

Answer the following questions by using a = 0.05:

A. Which month is the base month here (That is, the month when all dummy variables set to 0)?

B. Find the length of the time series (n)?