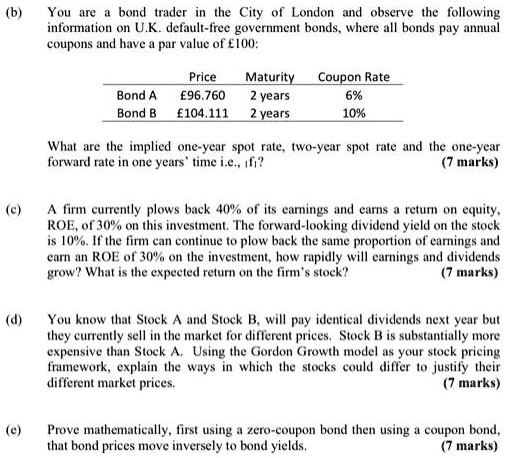

b) You are a bond trader in the City of London and observe the following information on U.K. default-free government bonds, where all bonds pay annual coupons and have a par value of £100:

Price Maturity Coupon Rate

Bond A £96.760 2 years 6%

Bond B £104.111 2 years 10%

What are the implied one-year spot rate, two-year spot rate and the one-year forward rate in one years' time i.e., $f_1$? (7 marks)

c) A firm currently plows back 40% of its earnings and earns a return on equity, ROE, of 30% on this investment. The forward-looking dividend yield on the stock is 10%. If the firm can continue to plow back the same proportion of earnings and earn an ROE of 30% on the investment, how rapidly will earnings and dividends grow? What is the expected return on the firm's stock? (7 marks)

d) You know that Stock A and Stock B, will pay identical dividends next year but they currently sell in the market for different prices. Stock B is substantially more expensive than Stock A. Using the Gordon Growth model as your stock pricing framework, explain the ways in which the stocks could differ to justify their different market prices. (7 marks)

e) Prove mathematically, first using a zero-coupon bond then using a coupon bond, that bond prices move inversely to bond yields. (7 marks)