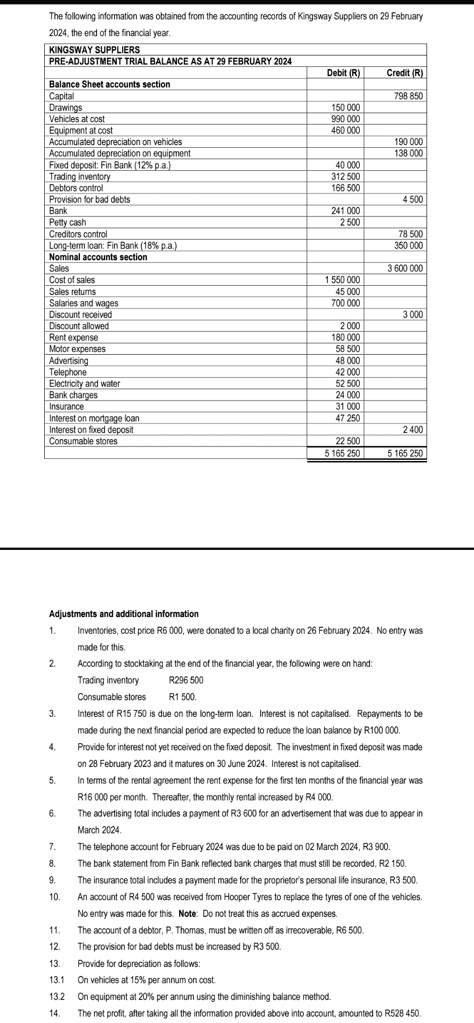

KINGSWAY SUPPLIERS

PRE-ADJUSTMENT TRIAL BALANCE AS AT 29 FEBRUARY 2024

Balance Sheet accounts section

Debit (R)

Credit (R)

Capital

798 850

Drawings

150 000

Vehicles at cost

990 000

Equipment at cost

460 000

Accumulated depreciation on vehicles

190 000

Accumulated depreciation on equipment

138 000

Fixed deposit: Fin Bank (12% p.a.)

40 000

Trading inventory

312 500

Debtors control

166 500

Provision for bad debts

4 500

Bank

241 000

Petty cash

2 500

Creditors control

78 500

Long-term loan: Fin Bank (18% p.a.)

350 000

Nominal accounts section

Sales

3 600 000

Cost of sales

1 550 000

Sales returns

45 000

Salaries and wages

700 000

Discount received

3 000

Discount allowed

2 000

Rent expense

180 000

Motor expenses

58 500

Advertising

48 000

Telephone

42 000

Electricity and water

52 500

Bank charges

24 000

Insurance

31 000

Interest on mortgage loan

47 250

Interest on fixed deposit

2 400

Consumable stores

22 500

5 165 250

5 165 250

Adjustments and additional information

1. Inventories, cost price R6 000, were donated to a local charity on 26 February 2024. No entry was made for this.

2. According to stocktaking at the end of the financial year, the following were on hand:

Trading inventory R296 500

Consumable stores R1 500.

3. Interest of R15 750 is due on the long-term loan. Interest is not capitalised. Repayments to be made during the next financial period are expected to reduce the loan balance by R100 000.

4. Provide for interest not yet received on the fixed deposit. The investment in fixed deposit was made on 28 February 2023 and it matures on 30 June 2024. Interest is not capitalised.

5. In terms of the rental agreement the rent expense for the first ten months of the financial year was R15 000 per month. Thereafter, the monthly rental increased by R4 000.

6. The advertising total includes a payment of R3 600 for an advertisement that was due to appear in March 2024.

7. The telephone account for February 2024 was due to be paid on 02 March 2024, R3 900.

8. The bank statement from Fin Bank reflected bank charges that must still be recorded, R2 150.

9. The insurance total includes a payment made for the proprietor's personal life insurance, R3 500.

10. An account of R4 500 was received from Hooper Tyres to replace the tyres of one of the vehicles. No entry was made for this. Note: Do not treat this as accrued expenses.

11. The account of a debtor, P. Thomas, must be written off as irrecoverable, R6 500.

12. The provision for bad debts must be increased by R3 500.

13. Provide for depreciation as follows:

13.1 On vehicles at 15% per annum on cost.

13.2 On equipment at 20% per annum using the diminishing balance method.

14. The net profit, after taking all the information provided above into account, amounted to R528 450.