27. On December 1, Zirbit Industries contracted to rent one of Omega's buildings. Zirbit paid

$48,000 in advance agreed for a two-year contract. Record Omega's adjusting entry on

December 31.

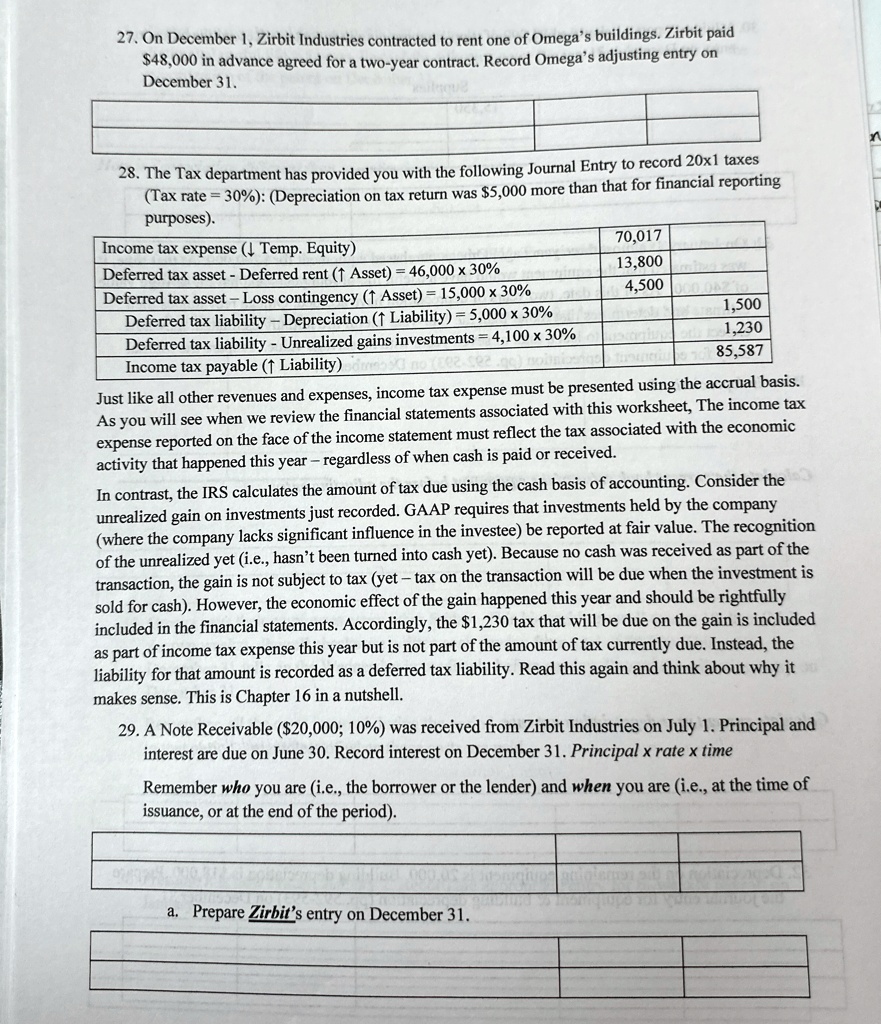

28. The Tax department has provided you with the following Journal Entry to record 20x1 taxes

(Tax rate = 30%): (Depreciation on tax return was $5,000 more than that for financial reporting

purposes).

Income tax expense (↓ Temp. Equity)

Deferred tax asset - Deferred rent (↑ Asset) = 46,000 x 30%

Deferred tax asset - Loss contingency (↑ Asset) = 15,000 x 30%

Deferred tax liability - Depreciation (↑ Liability) = 5,000 x 30%

Deferred tax liability - Unrealized gains investments = 4,100 x 30%

Income tax payable (↑ Liability)

70,017

13,800

4,500

1,500

1,230

85,587

Just like all other revenues and expenses, income tax expense must be presented using the accrual basis.

As you will see when we review the financial statements associated with this worksheet, The income tax

expense reported on the face of the income statement must reflect the tax associated with the economic

activity that happened this year - regardless of when cash is paid or received.

In contrast, the IRS calculates the amount of tax due using the cash basis of accounting. Consider the

unrealized gain on investments just recorded. GAAP requires that investments held by the company

(where the company any lacks significant influence in the investee) be reported at fair value. The recognition

of the unrealized yet (i.e., hasn't been turned into cash yet). Because no cash was received as part of the

transaction, the gain is not subject to tax (yet - tax on the transaction will be due when the investment is

sold for cash). However, the economic effect of the gain happened this year and should be rightfully

included in the financial statements. Accordingly, the $1,230 tax that will be due on the gain is included

as part of income tax expense this year but is not part of the amount of tax currently due. Instead, the

liability for that amount is recorded as a deferred tax liability. Read this again and think about why it

makes sense. This is Chapter 16 in a nutshell.

29. A Note Receivable ($20,000; 10%) was received from Zirbit Industries on July 1. Principal and

interest are due on June 30. Record interest on December 31. Principal x rate x time

Remember who you are (i.e., the borrower or the lender) and when you are (i.e., at the time of

issuance, or at the end of the period).

a. Prepare Zirbit's entry on December 31.