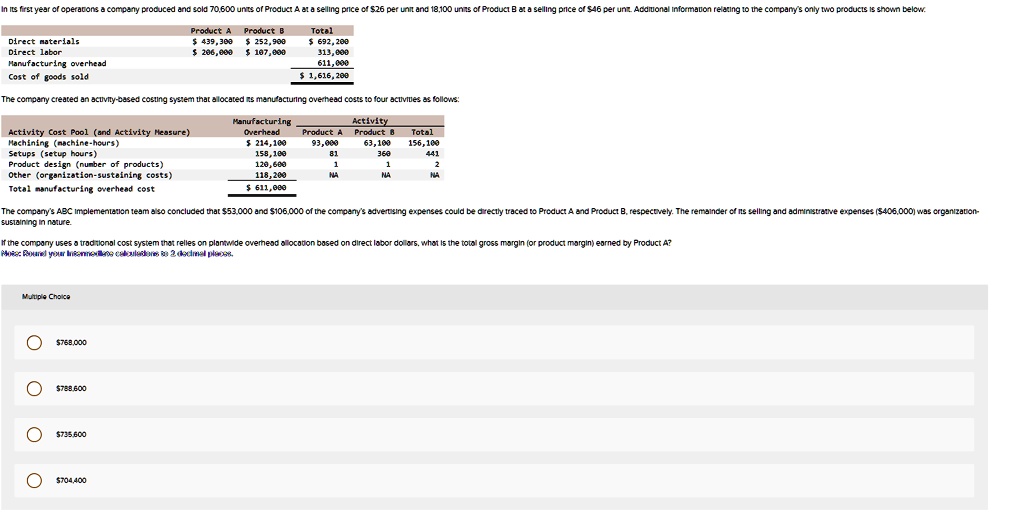

In Its first year of operations a company produced and sold 70,600 units of Product A at a selling price of $26 per unit and 18,100 units of Product B at a selling price of $46 per unit. Additional information relating to the company's only two products is shown below.

Direct materials

Direct labor

Manufacturing overhead

Cost of goods sold

Product A

Product B

Total

$\ 439,300

$\ 252,900

$\ 692,200

$\ 206,000

$\ 107,000

$\ 313,000

$\ 611,000

$\ 1,616,200

The company created an activity-based costing system that allocated its manufacturing overhead costs to four activities as follows:

Manufacturing

Activity

Activity Cost Pool (and Activity Measure)

Overhead

Product A

Product B

Total

Machining (machine-hours)

$\ 214,100

93,000

63,100

156,100

Setups (setup hours)

$\ 158,100

81

360

441

Product design (number of products)

$\ 120,600

1

1

2

Other (organization-sustaining costs)

$\ 118,200

NA

NA

NA

Total manufacturing overhead cost

$\ 611,000

The company's ABC Implementation team also concluded that $53,000 and $106,000 of the company's advertising expenses could be directly traced to Product A and Product B, respectively. The remainder of its selling and administrative expenses ($406,000) was organization-

sustaining in nature.

If the company uses a traditional cost system that relies on plantwide overhead allocation based on direct labor dollars, what is the total gross margin (or product margin) earned by Product A?

Note: Round your intermediate calculations to 2 decimal places.

Multiple Choice

$\ 768,000

$\ 788,600

$\ 735,600

$\ 704,400