Part 2: Lower-of-Cost-or-Market Value

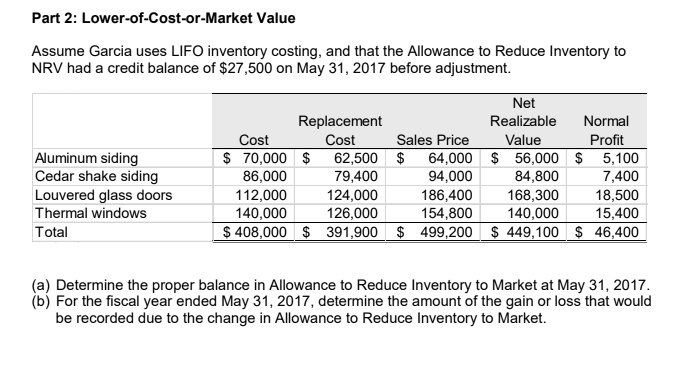

Assume Garcia uses LIFO inventory costing, and that the Allowance to Reduce Inventory to

NRV had a credit balance of $27,500 on May 31, 2017 before adjustment.

Cost

Replacement

Cost

Net

Realizable

Normal

Sales Price Value

Profit

Aluminum siding

$ 70,000 $ 62,500 $ 64,000 $ 56,000 $ 5,100

Cedar shake siding

86,000

79,400

94,000 84,800

7,400

Louvered glass doors

112,000

124,000

186,400

168,300

18,500

Thermal windows

140,000

126,000

154,800 140,000 15,400

Total

$408,000 $ 391,900 $ 499,200 $ 449,100 $ 46,400

(a) Determine the proper balance in Allowance to Reduce Inventory to Market at May 31, 2017.

(b) For the fiscal year ended May 31, 2017, determine the amount of the gain or loss that would

be recorded due to the change in Allowance to Reduce Inventory to Market.