Consider the following multiple linear regression model:

y_t = β_1 + β_2x_2t + β_3x_3t + β_4x_4t + β_5x_5t + u_t, t = 1, ..., T.

Assume that Var(u) = σ^2I_T, where u = (u_1, ..., u_T)'. We want to test

H_0: β_2 = β_3 = β_4 = β_5 = 0 against H_1: H_0 is not true.

Let RRSS be the residual sum of squares from the restricted model under H_0, and let URSS be the residual sum of squares from the unrestricted model. Use the following approximate quantiles of χ^2(m) whenever it is necessary.

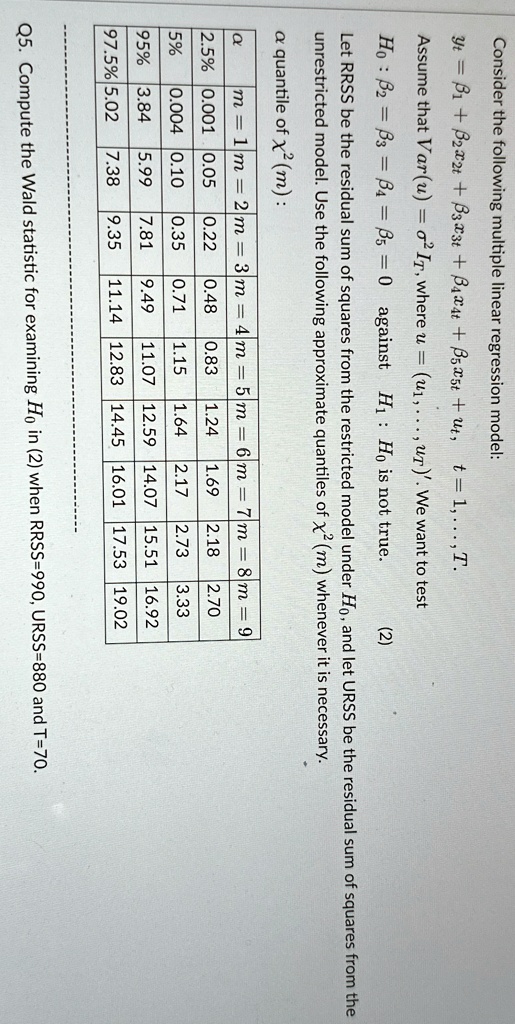

α quantile of χ^2(m):

[

�egin{array}{|c|c|c|c|c|c|c|c|c|c|}

hline

alpha & m=1 & m=2 & m=3 & m=4 & m=5 & m=6 & m=7 & m=8 & m=9 \

hline

97.5% & 5.02 & 5.99 & 0.004 & 0.10 & 0.001 & 0.05 \

hline

end{array}

]

quantile of χ^2(m): 9.35 7.81 0.35 9.49 0.71 0.22 11.14 0.48

Ho: β_3 = β_4 = 0 against H: Ho is not true. y_t = β_2x_2t + β_3x_3t + β_4x_4t + x_5t + u_t, t = 1, T. Consider the following multiple linear regression model: Q5. Compute the Wald statistic for examining Ho in (2) when RRSS = 990, URSS = 880 and T = 70. 11.07 1.15 1.24 0.83 1.64 6 = u | 8 = u = u g = u | g = u | b = u 8 = u 2 = u I = u 12.59 unrestricted model. Use the following approximate quantiles of χ^2(m) whenever it is necessary. 12.83 14.45 16.01 17.53 19.02 14.07 2.17 1.69 15.51 2.73 2.18 Let RRSS be the residual sum of squares from the restricted model under Ho, and let URSS be the residual sum of squares from the 16.92 3.33 2.70 2