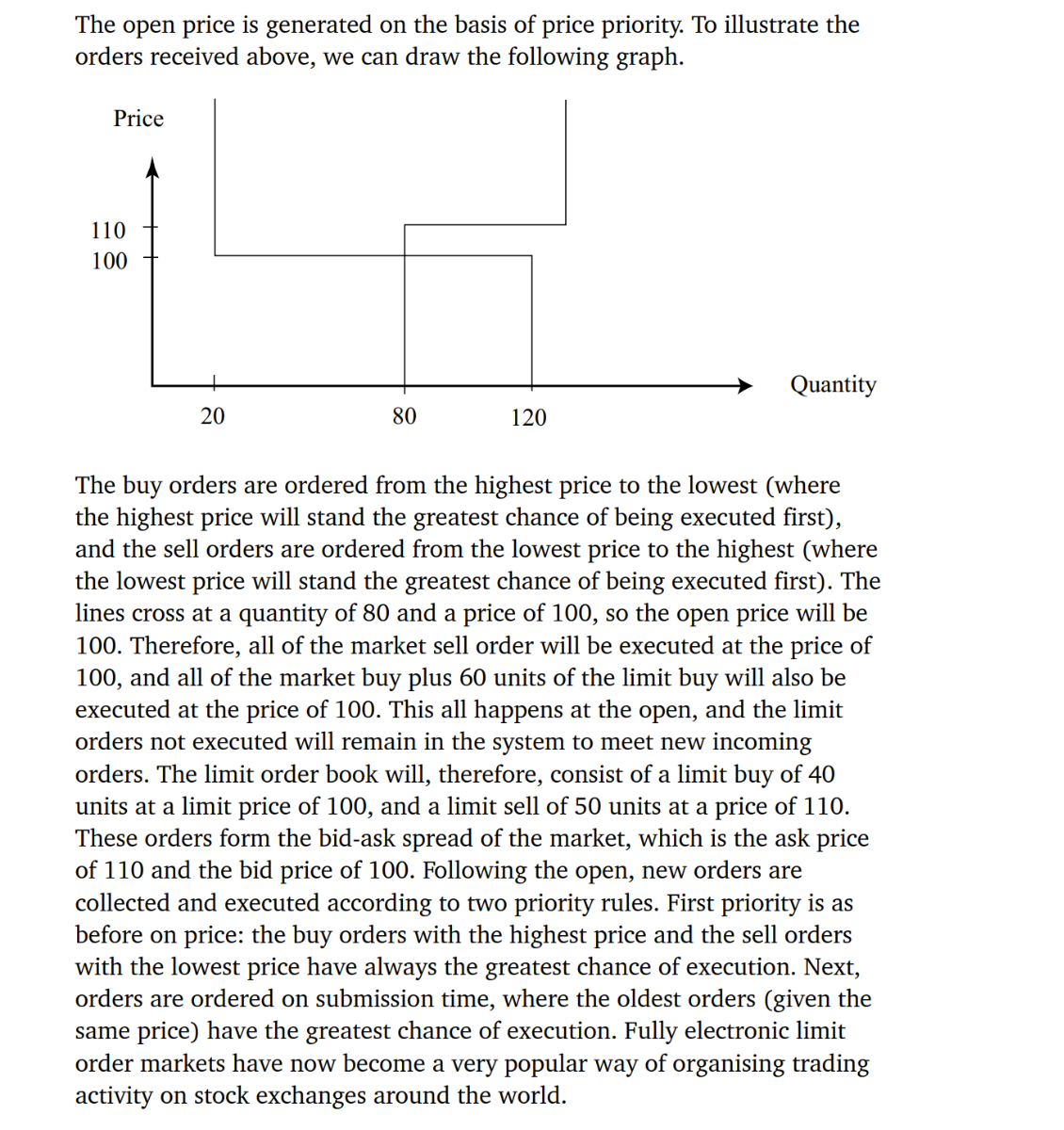

The open price is generated on the basis of price priority. To illustrate the orders received above, we can draw the following graph.

The buy orders are ordered from the highest price to the lowest (where the highest price will stand the greatest chance of being executed first), and the sell orders are ordered from the lowest price to the highest (where the lowest price will stand the greatest chance of being executed first). The lines cross at a quantity of 80 and a price of 100 , so the open price will be 100. Therefore, all of the market sell order will be executed at the price of 100 , and all of the market buy plus 60 units of the limit buy will also be executed at the price of 100 . This all happens at the open, and the limit orders not executed will remain in the system to meet new incoming orders. The limit order book will, therefore, consist of a limit buy of 40 units at a limit price of 100, and a limit sell of 50 units at a price of 110 . These orders form the bid-ask spread of the market, which is the ask price of 110 and the bid price of 100 . Following the open, new orders are collected and executed according to two priority rules. First priority is as before on price: the buy orders with the highest price and the sell orders with the lowest price have always the greatest chance of execution. Next, orders are ordered on submission time, where the oldest orders (given the same price) have the greatest chance of execution. Fully electronic limit order markets have now become a very popular way of organising trading activity on stock exchanges around the world.