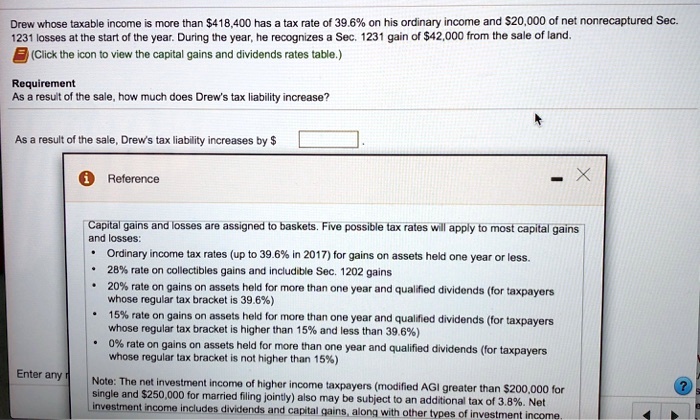

Drew, whose taxable income is more than $418,400, has a tax rate of 39.6% on his ordinary income and $20,000 of net nonrecaptured Sec. 1231 losses at the start of the year. During the year, he recognizes a Sec. 1231 gain of $42,000 from the sale of land. (Click the icon to view the capital gains and dividends rates table.)

Requirement: As a result of the sale, how much does Drew's tax liability increase?

As a result of the sale, Drew's tax liability increases by $

Reference on gains and losses:

- 28% rate on collectibles gains and includible Sec. 1202 gains

- 20% rate on gains on assets held for more than one year and qualified dividends (for taxpayers whose regular tax bracket is 39.6%)

- 15% rate on gains on assets held for more than one year and qualified dividends (for taxpayers whose regular tax bracket is higher than 15% and less than 39.6%)

- 0% rate on gains on assets held for more than one year and qualified dividends (for taxpayers whose regular tax bracket is not higher than 15%)

Note: The net investment income of higher income taxpayers (modified AGI greater than $200,000 for single and $250,000 for married filing jointly) may also be subject to an additional tax of 3.8%. Net investment income includes dividends and capital gains, along with other types of investment income.

Enter any