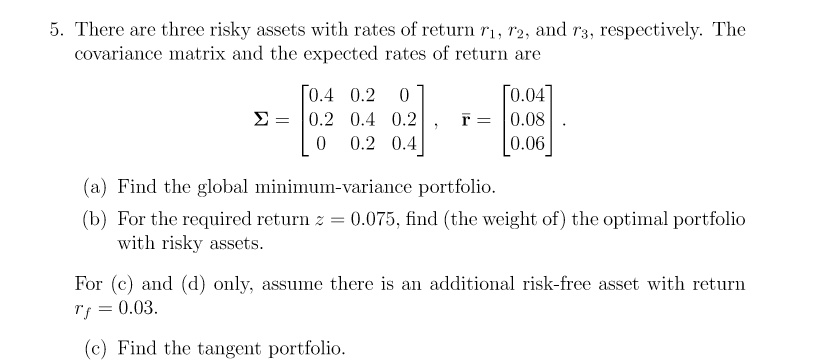

5. There are three risky assets with rates of return $r_1$, $r_2$, and $r_3$, respectively. The covariance matrix and the expected rates of return are

$\Sigma = \begin{bmatrix} 0.4 & 0.2 & 0\\ 0.2 & 0.4 & 0.2\\ 0 & 0.2 & 0.4 \end{bmatrix}$, $\bar{r} = \begin{bmatrix} 0.04\\ 0.08\\ 0.06 \end{bmatrix}$.

(a) Find the global minimum-variance portfolio.

(b) For the required return $z = 0.075$, find (the weight of) the optimal portfolio with risky assets.

For (c) and (d) only, assume there is an additional risk-free asset with return $r_f = 0.03$.

(c) Find the tangent portfolio.