The following information relates to questions 2,3 and 4.

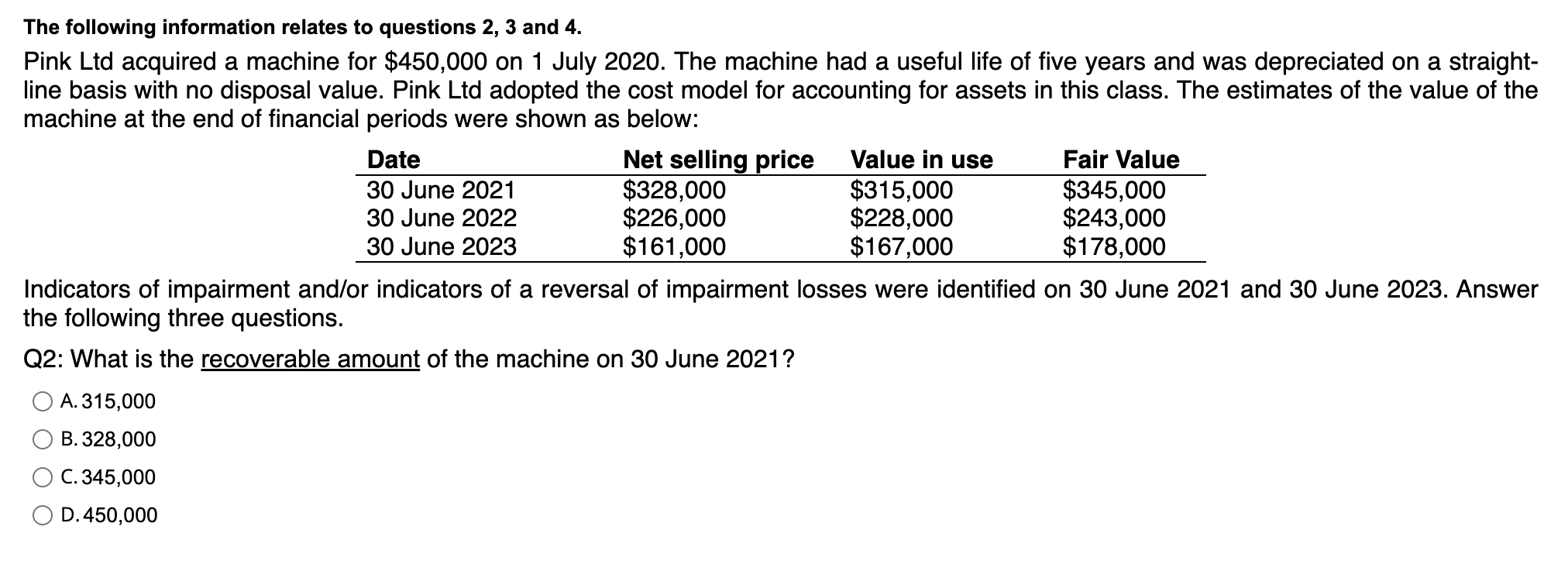

Pink Ltd acquired a machine for \( \$ 450,000 \) on 1 July 2020 . The machine had a useful life of five years and was depreciated on a straightline basis with no disposal value. Pink Ltd adopted the cost model for accounting for assets in this class. The estimates of the value of the machine at the end of financial periods were shown as below:

\begin{tabular}{llll}

Date & Net selling price & Value in use & Fair Value \\

\hline 30 June 2021 & \( \$ 328,000 \) & \( \$ 315,000 \) & \( \$ 345,000 \) \\

30 June 2022 & \( \$ 226,000 \) & \( \$ 228,000 \) & \( \$ 243,000 \) \\

30 June 2023 & \( \$ 161,000 \) & \( \$ 167,000 \) & \( \$ 178,000 \) \\

\hline

\end{tabular}

Indicators of impairment and/or indicators of a reversal of impairment losses were identified on 30 June 2021 and 30 June 2023 . Answer the following three questions.

Q2: What is the recoverable amount of the machine on 30 June 2021 ?

A. 315,000

B. 328,000

C. 345,000

D. 450,000