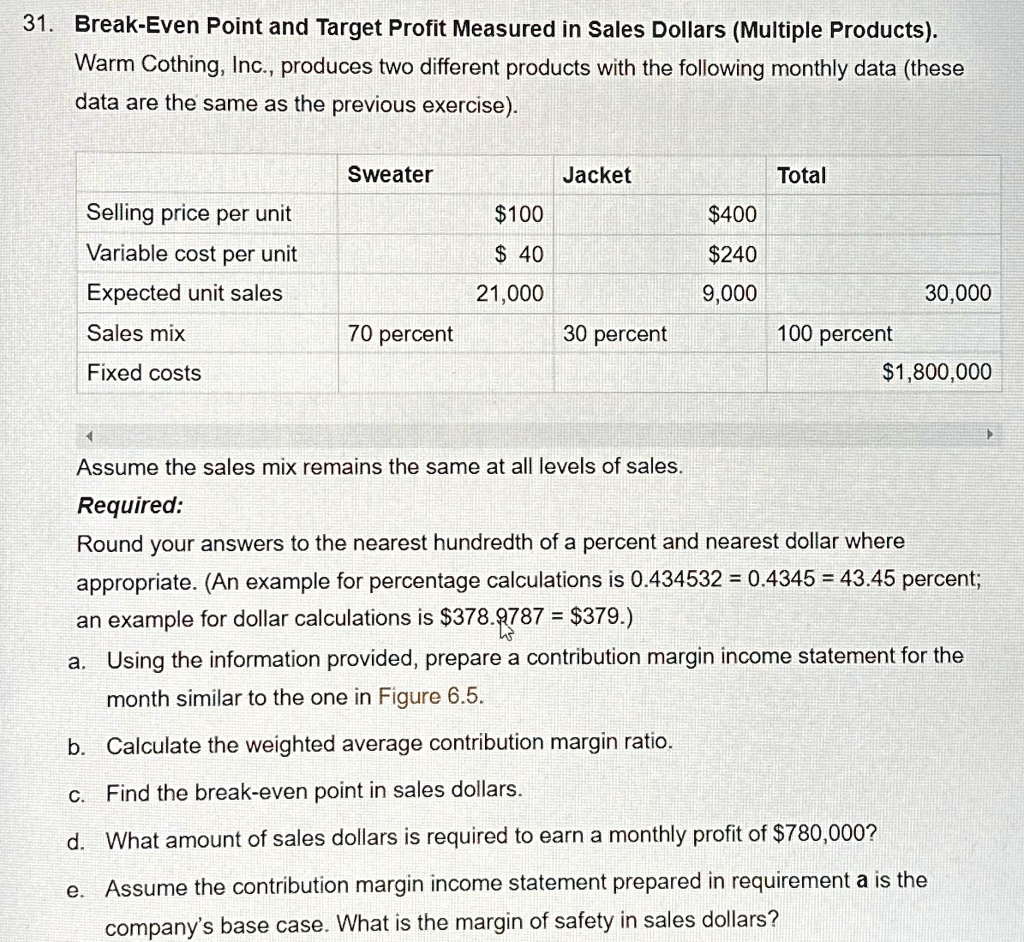

Break-Even Point and Target Profit Measured in Sales Dollars (Multiple Products). Warm Clothing, Inc., produces two different products with the following monthly data (these data are the same as the previous exercise).

[

�egin{array}{|c|c|c|}

hline

& ext{Sweater} & ext{Jacket} & ext{Total} \

hline

ext{Selling price per unit} & $100 & $400 & \

ext{Variable cost per unit} & $40 & $240 & \

ext{Expected unit sales} & 21,000 & 9,000 & 30,000 \

ext{Sales mix} & 70% & 30% & 100% \

ext{Fixed costs} & & & $1,800,000 \

hline

end{array}

]

31. Break-Even Point and Target Profit Measured in Sales Dollars (Multiple Products) Warm Clothing, Inc., produces two different products with the following monthly data (these data are the same as the previous exercise).

Sweater

Jacket $100 $40 21,000 70 percent 30 percent

Total $400 $240 9,000 30,000 100 percent $1,800,000

Selling price per unit Variable cost per unit Expected unit sales

Sales mix

Fixed costs

Assume the sales mix remains the same at all levels of sales.

Required: Round your answers to the nearest hundredth of a percent and nearest dollar where appropriate. (An example for percentage calculations is 0.434532 = 0.4345 = 43.45 percent; an example for dollar calculations is $378.9787 = $379.)

a. Using the information provided, prepare a contribution margin income statement for the month similar to the one in Figure 6.5.

b. Calculate the weighted average contribution margin ratio.

c. Find the break-even point in sales dollars.

d. What amount of sales dollars is required to earn a monthly profit of $780,000?

e. Assume the contribution margin income statement prepared in requirement a is the company's base case. What is the margin of safety in sales dollars?