Texts: ZorZpages

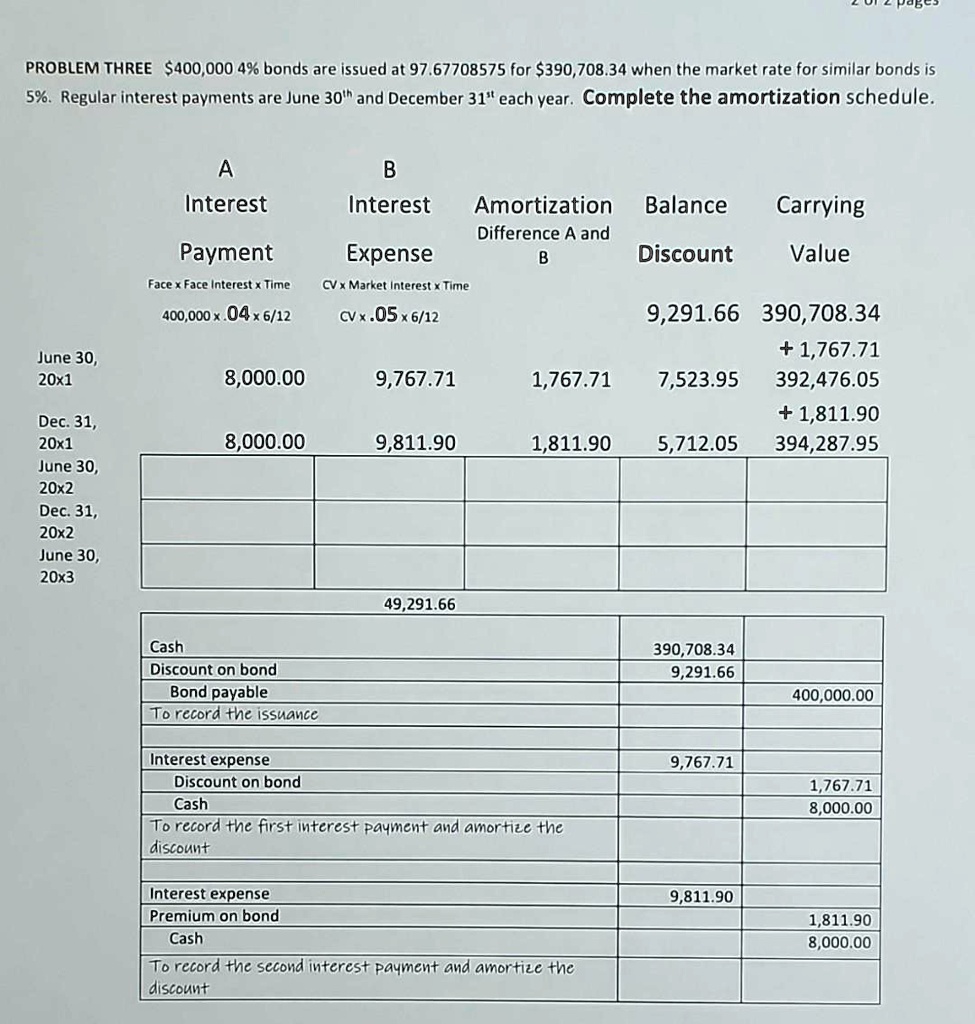

PROBLEM THREE: $400,000 4% bonds are issued at 97.67708575 for $390,708.34 when the market rate for similar bonds is 5%. Regular interest payments are on June 30th and December 31st each year. Complete the amortization schedule.

A

B

Interest

Interest

Amortization Balance Carrying Difference A and Payment Expense B Discount Value Face x Face Interest x Time CV x Market interest x Time 400,000.046/12 CV.056/12 9,291.66 390,708.34 +1,767.71 8,000.00 9,767.71 1,767.71 7,523.95 392,476.05

June 30, 20x1

Dec. 31, 20x1

June 30, 20x2

Dec. 31, 20x2

June 30, 203

+1,811.90 394,287.95

8,000.00

9,811.90

1,811.90

5,712.05

49,291.66

Cash Discount on bond Bond payable To record the issuance

390,708.34 9,291.66

400,000.00

Interest expense Discount on bond Cash To record the first interest payment and amortize the discount

9,767.71

1,767.71

8,000.00

Interest expense Premium on bond Cash To record the second interest payment and amortize the discount

9,811.90

1,811.90

8,000.00