Khumalo Enterprises manufactures a single product, and the management accountant has produced

the following budget:

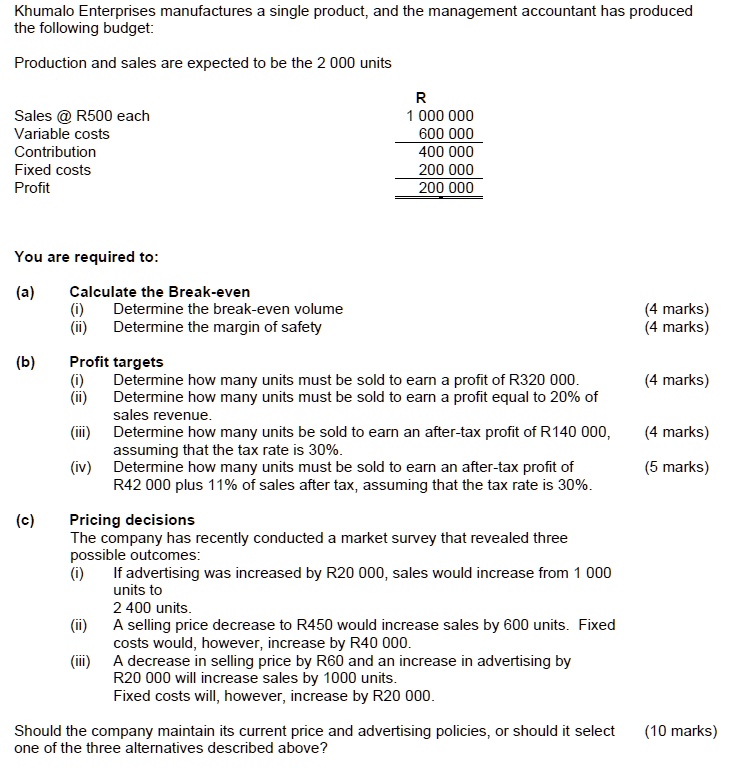

Production and sales are expected to be the 2 000 units

Sales @ R500 each

Variable costs

Contribution

Fixed costs

Profit

R

1 000 000

600 000

400 000

200 000

200 000

You are required to:

(a)

Calculate the Break-even

(i)

Determine the break-even volume

(4 marks)

(ii)

Determine the margin of safety

(4 marks)

(b)

Profit targets

(i)

Determine how many units must be sold to earn a profit of R320 000.

(4 marks)

(ii)

Determine how many units must be sold to earn a profit equal to 20% of

sales revenue.

(4 marks)

(iii)

Determine how many units be sold to earn an after-tax profit of R140 000,

assuming that the tax rate is 30%.

(5 marks)

(iv) Determine how many units must be sold to earn an after-tax profit of

R42 000 plus 11% of sales after tax, assuming that the tax rate is 30%.

(c)

Pricing decisions

The company has recently conducted a market survey that revealed three

possible outcomes:

(i)

If advertising was increased by R20 000, sales would increase from 1 000

units to

2 400 units.

(ii)

A selling price decrease to R450 would increase sales by 600 units. Fixed

costs would, however, increase by R40 000.

(iii)

A decrease in selling price by R60 and an increase in advertising by

R20 000 will increase sales by 1000 units.

Fixed costs will, however, increase by R20 000.

Should the company maintain its current price and advertising policies, or should it select (10 marks)

one of the three alternatives described above?