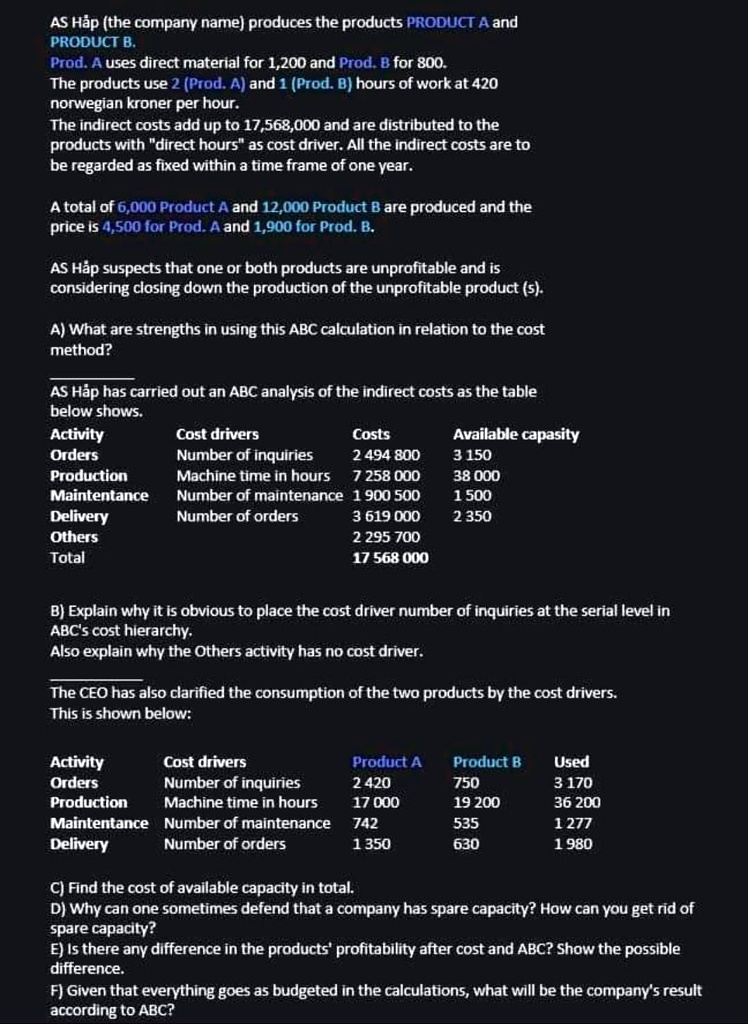

AS Hap (the company name) produces the products PRODUCT A and PRODUCT B.

Prod. A uses direct material for 1,200 and Prod. B for 800. The products use 2 Prod. A and 1 Prod. B hours of work at 420 Norwegian kroner per hour. The indirect costs add up to 17,568,000 and are distributed to the products with "direct hours" as the cost driver. All the indirect costs are to be regarded as fixed within a time frame of one year.

A total of 6,000 Product A and 12,000 Product B are produced and the price is 4,500 for Prod. A and 1,900 for Prod. B.

AS Hap suspects that one or both products are unprofitable and is considering closing down the production of the unprofitable product(s).

A. What are the strengths in using this ABC calculation in relation to the cost method?

AS Hap has carried out an ABC analysis of the indirect costs as the table below shows:

Activity Cost drivers Costs Available capacity Orders Number of inquiries 2,494,800 3,150 Production Machine time in hours 7,258,000 38,000 Maintenance Number of maintenance 1,900,500 1,500 Delivery Number of orders 3,519,000 2,350 Others 2,295,700 Total 17,568,000

B. Explain why it is obvious to place the cost driver "number of inquiries" at the serial level in ABC's cost hierarchy. Also, explain why the "Others" activity has no cost driver.

The CEO has also clarified the consumption of the two products by the cost drivers. This is shown below:

Activity Cost drivers Orders Number of inquiries Production Machine time in hours Maintenance Number of maintenance Delivery Number of orders

Product A 2,420 17,000 742 1,350

Product B 750 19,200 535 630

Used 3,170 36,200 1,277 1,980

C) Find the cost of available capacity in total.

D) Why can one sometimes defend that a company has spare capacity? How can you get rid of spare capacity?

E) Is there any difference in the products' profitability after cost and ABC? Show the possible difference.

F) Given that everything goes as budgeted in the calculations, what will be the company's result according to ABC?