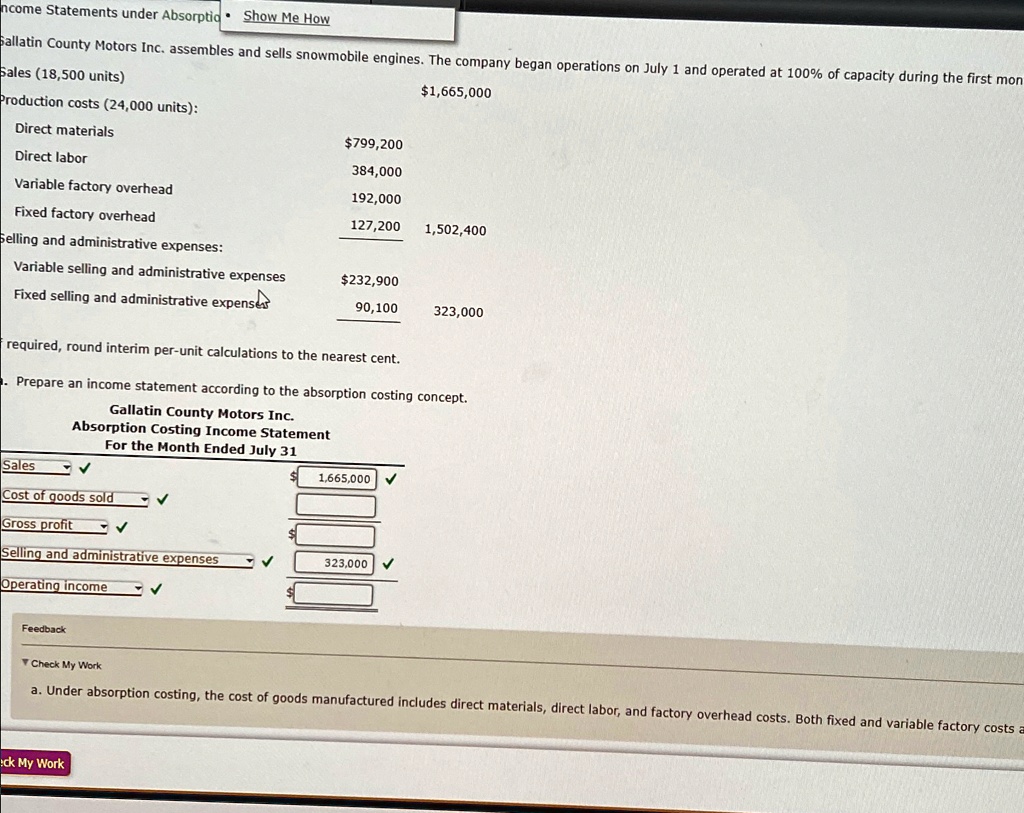

a. Under absorption costing, the cost of goods manufactured includes direct materials, direct labor, and factory overhead costs. Both fixed and variable factory costs are included in the calculation of the cost of goods sold.

Sales: $1,665,000

Production costs: $799,200 (direct materials) + $384,000 (direct labor) + $192,000 (variable factory overhead) + $127,200 (fixed factory overhead) = $1,502,400

Gross profit: Sales - Cost of goods sold = $1,665,000 - $1,502,400 = $162,600

Selling and administrative expenses: $232,900 (variable) + $90,100 (fixed) = $323,000

Operating income: Gross profit - Selling and administrative expenses = $162,600 - $323,000 = -$160,400