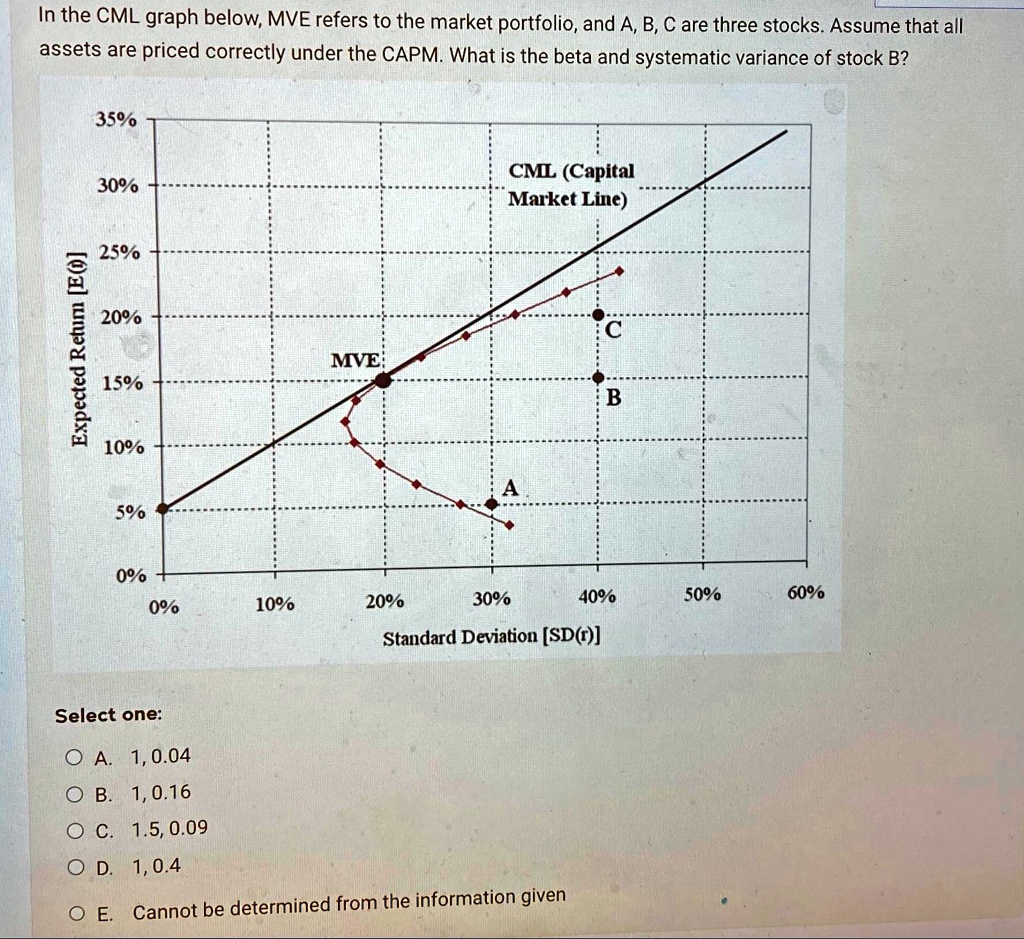

In the CML graph below, MVE refers to the market portfolio, and A, B, C are three stocks. Assume that all assets are priced correctly under the CAPM. What is the beta and systematic variance of stock B?

35%

Expected Return [E(r)]

30%

25%

CML (Capital

Market Line)

20%

C

MVE

15%

B

10%

5%

A

0%

0%

10%

20%

30%

40%

50%

60%

Standard Deviation [SD(r)]

Select one:

? A. 1, 0.04

? B. 1, 0.16

? C. 1.5, 0.09

? D. 1, 0.4

? E. Cannot be determined from the information given