Question 9

The following are the financial statements of White and its subsidiary Brown as at 30 September 20X9

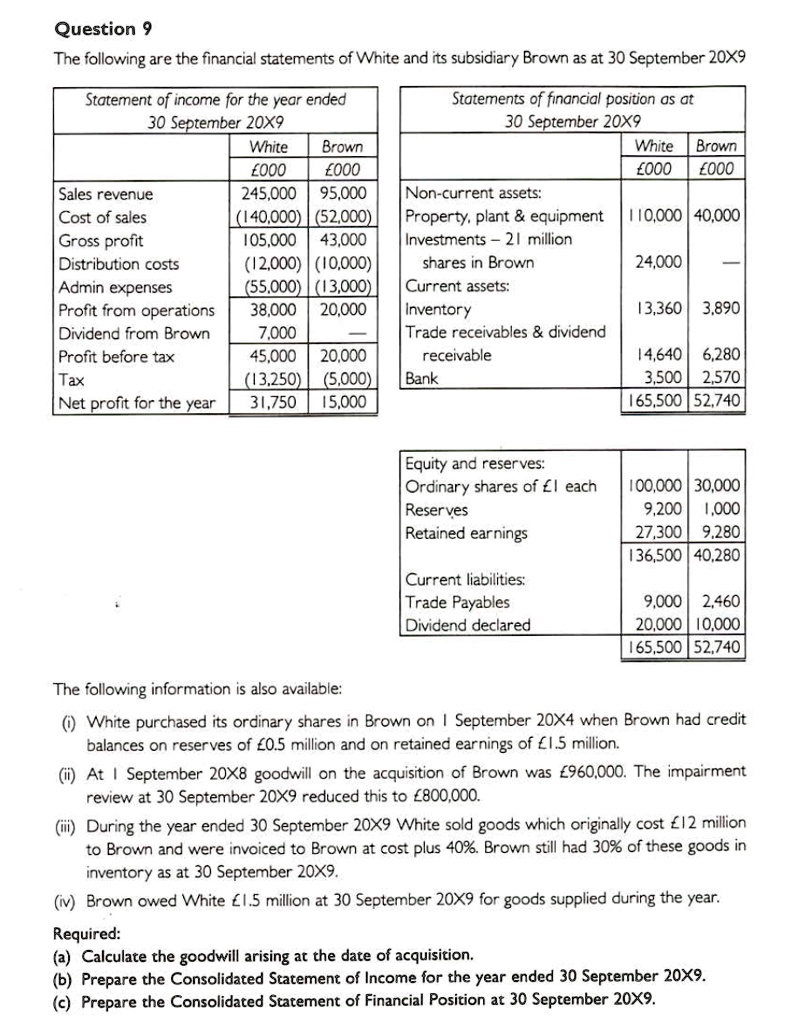

Statement of income for the year ended

30 September 20X9

White Brown

£000 £000

Sales revenue 245,000 95,000

Cost of sales (140,000) (52,000)

Gross profit 105,000 43,000

Distribution costs (12,000) (10,000)

Admin expenses (55,000) (13,000)

Profit from operations 38,000 20,000

Dividend from Brown 7,000 —

Profit before tax 45,000 20,000

Tax (13,250) (5,000)

Net profit for the year 31,750 15,000

Statements of financial position as at

30 September 20X9

White Brown

£000 £000

Non-current assets:

Property, plant & equipment 110,000 40,000

Investments – 21 million

shares in Brown 24,000 —

Current assets:

Inventory 13,360 3,890

Trade receivables & dividend

receivable 14,640 6,280

Bank 3,500 2,570

165,500 52,740

Equity and reserves:

Ordinary shares of £1 each 100,000 30,000

Reserves 9,200 1,000

Retained earnings 27,300 9,280

136,500 40,280

Current liabilities:

Trade Payables 9,000 2,460

Dividend declared 20,000 10,000

165,500 52,740

The following information is also available:

(i) White purchased its ordinary shares in Brown on 1 September 20X4 when Brown had credit balances on reserves of £0.5 million and on retained earnings of £1.5 million.

(ii) At 1 September 20X8 goodwill on the acquisition of Brown was £960,000. The impairment review at 30 September 20X9 reduced this to £800,000.

(iii) During the year ended 30 September 20X9 White sold goods which originally cost £12 million to Brown and were invoiced to Brown at cost plus 40%. Brown still had 30% of these goods in inventory as at 30 September 20X9.

(iv) Brown owed White £1.5 million at 30 September 20X9 for goods supplied during the year.

Required:

(a) Calculate the goodwill arising at the date of acquisition.

(b) Prepare the Consolidated Statement of Income for the year ended 30 September 20X9.

(c) Prepare the Consolidated Statement of Financial Position at 30 September 20X9.