4KPlay Inc. manufactures and sells 50-inch television sets and uses standard costing. Actual data relating to January, February, and March are as follows.

(Click to view the data.)

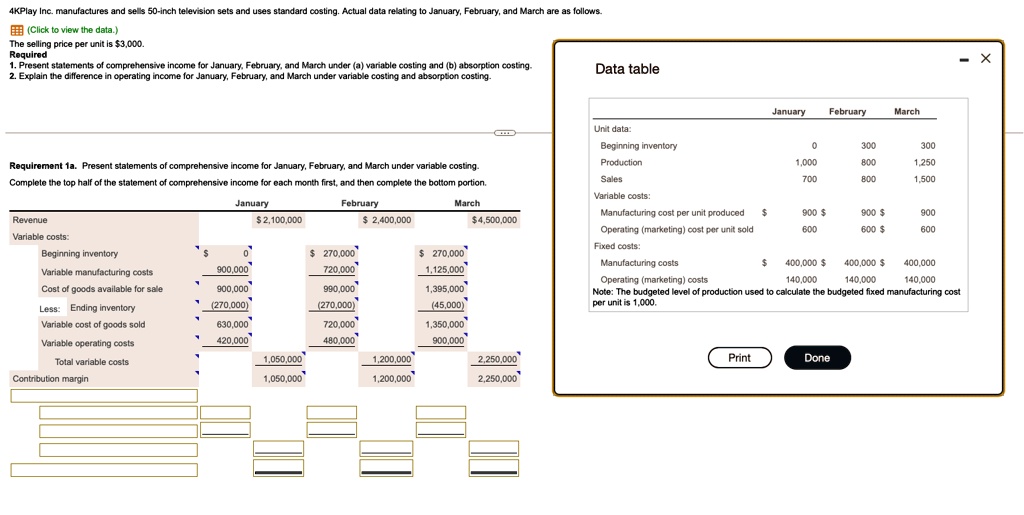

The selling price per unit is $3,000.

Required

1. Present statements of comprehensive income for January, February, and March under (a) variable costing and (b) absorption costing.

2. Explain the difference in operating income for January, February, and March under variable costing and absorption costing.

Data table

January February March

Unit data:

Beginning inventory 0 300 300

Production 1,000 800 1,250

Sales 700 800 1,500

Variable costs:

Manufacturing cost per unit produced $ 900 $ 900 $ 900

Operating (marketing) cost per unit sold 600 600 $ 600

Fixed costs:

Manufacturing costs $ 400.000 $ 400,000 $ 400,000

Operating (marketing) costs 140,000 140,000 140,000

Note: The budgeted level of production used to calculate the budgeted fixed manufacturing cost per unit is 1,000.

Requirement 1a. Present statements of comprehensive income for January, February, and March under variable costing.

Complete the top half of the statement of comprehensive income for each month first, and then complete the bottom portion.

January February March

Revenue $2,100,000 $ 2,400,000 $4,500,000

Variable costs:

Beginning inventory $ 0 $ 270,000 $ 270,000

Variable manufacturing costs 900,000 720,000 1,125,000

Cost of goods available for sale 900,000 990,000 1,395,000

Less: Ending inventory (270,000) (270,000) (45,000)

Variable cost of goods sold 630,000 720,000 1,350,000

Variable operating costs 420,000 480,000 900,000

Total variable costs 1,050,000 1,200,000 2,250,000

Contribution margin 1,050,000 1,200,000 2,250,000