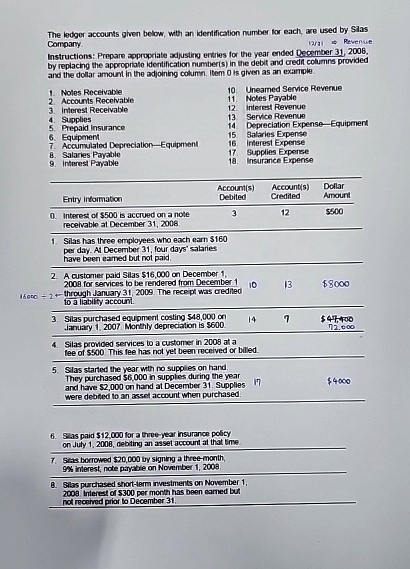

The ledger accounts given below, with an identification number for each, are used by Silas Company.

Instructions: Prepare appropriate adjusting entries for the year ended December 31, 2008, by replacing the appropriate identification number(s) in the debit and credit columns provided and the dollar amount in the adjoining column. Item 0 is given as an example.

1. Notes Receivable

2. Accounts Receivable

3. Interest Receivable

4. Supplies

5. Prepaid Insurance

6. Equipment

7. Accumulated Depreciation-Equipment

8. Salaries Payable

9. Interest Payable

10. Unearned Service Revenue

11. Notes Payable

12. Interest Revenue

13. Service Revenue

14. Depreciation Expense-Equipment

15. Salaries Expense

16. Interest Expense

17. Supplies Expense

18. Insurance Expense

Entry information

0. Interest of $500 is accrued on a note receivable at December 31, 2008.

1. Silas has three employees who each earn $160 per day. At December 31, four days' salaries have been earned but not paid.

2. A customer paid Silas $16,000 on December 1, 2008 for services to be rendered from December 1 through January 31, 2009. The receipt was credited to a liability account.

3. Silas purchased equipment costing $48,000 on January 1, 2007. Monthly depreciation is $600.

4. Silas provided services to a customer in 2008 at a fee of $500. This fee has not yet been received or billed.

5. Silas started the year with no supplies on hand. They purchased $6,000 in supplies during the year and have $2,000 on hand at December 31. Supplies were debited to an asset account when purchased.

6. Silas paid $12,000 for a three-year insurance policy on July 1, 2008, debiting an asset account at that time.

7. Silas borrowed $20,000 by signing a three-month, 9% interest, note payable on November 1, 2008.

8. Silas purchased short-term investments on November 1, 2008. Interest of $300 per month has been earned but not received prior to December 31.

Account(s) Debited Account(s) Credited Dollar Amount

3 12 $500

10 13 $8000

14 7 $47,400

17 $4000