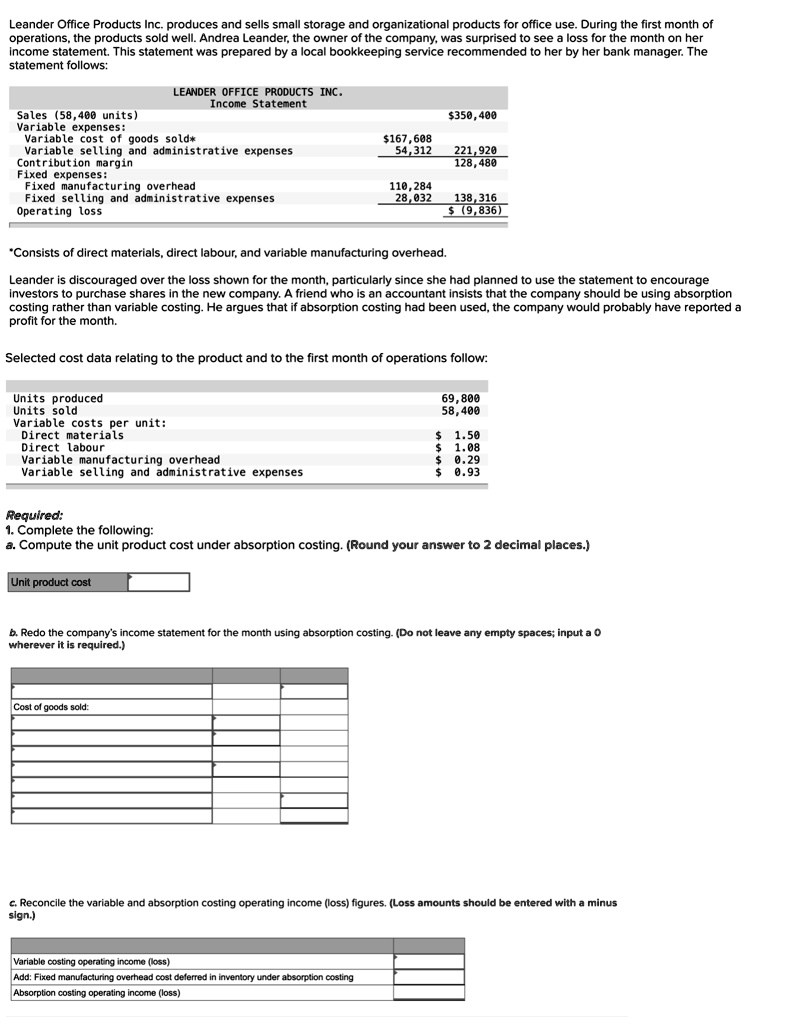

Leander Office Products Inc. produces and sells small storage and organizational products for office use. During the first month of

operations, the products sold well. Andrea Leander, the owner of the company, was surprised to see a loss for the month on her

income statement. This statement was prepared by a local bookkeeping service recommended to her by her bank manager. The

statement follows:

Sales (58,400 units)

Variable expenses:

LEANDER OFFICE PRODUCTS INC.

Variable cost of goods sold*

Income Statement

Variable selling and administrative expenses

Contribution margin

Fixed expenses:

Fixed manufacturing overhead

Fixed selling and administrative expenses

Operating loss

$350,400

$167,608

54,312 221,920

128,480

110,284

28,032

138,316

$ (9,836)

*Consists of direct materials, direct labour, and variable manufacturing overhead.

Leander is discouraged over the loss shown for the month, particularly since she had planned to use the statement to encourage

investors to purchase shares in the new company. A friend who is an accountant insists that the company should be using absorption

costing rather than variable costing. He argues that if absorption costing had been used, the company would probably have reported a

profit for the month.

Selected cost data relating to the product and to the first month of operations follow:

Units produced

Units sold

Variable costs per unit:

Direct materials

Direct labour

Variable manufacturing overhead

Variable selling and administrative expenses

Required:

1. Complete the following:

a. Compute the unit product cost under absorption costing. (Round your answer to 2 decimal places.)

Unit product cost

b. Redo the company's income statement for the month using absorption costing. (Do not leave any empty spaces; input a 0

wherever it is required.)

Cost of goods sold:

c. Reconcile the variable and absorption costing operating income (loss) figures. (Loss amounts should be entered with a minus

sign.)

Variable costing operating income (loss)

Add: Fixed manufacturing overhead cost deferred in inventory under absorption costing

Absorption costing operating income (loss)

69,800

58,400

$ 1.50

$ 1.08

$ 0.29

$ 0.93