Texts: Remember that a shareholder is taxed on S corporation income whether withdrawn or not and is not taxed on the actual withdrawals or distributions. Assume the C corporation is in the 21% corporate tax bracket, Calliah is in the 22% individual tax bracket for ordinary income, and Calliah is taxed at 15% on dividend income. When considering either corporate option, perform the analysis first by treating any withdrawals as deductible salary payments of the corporation. Then do the analysis by treating them as nondeductible dividends or distributions. Ignore employment and self-employment taxes.

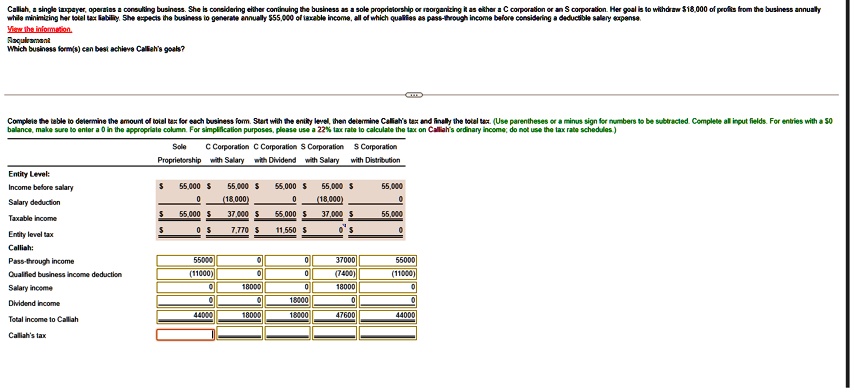

Calliah, a single taxpayer, operates a consulting business. She is considering either continuing the business as a sole proprietorship or reorganizing it as either a C corporation or an S corporation. Her goal is to withdraw $18,000 of profits from the business annually while minimizing her total tax liability. She expects the business to generate annually $55,000 of taxable income, all of which qualifies as pass-through income before considering a deductible salary expense. Use the information provided to determine which business form(s) can best achieve Calliah's goals.

Complete the table to determine the amount of total tax for each form. Start with the entity level, then determine Calliah's tax.

Sole

Proprietorship C Corporation C Corporation S Corporation S Corporation with Salary with Dividend with Salary with Distribution

Entity Level: Income before salary Salary deduction Taxable income Entity level tax Calliah: Pass-through income Qualified business income deduction Salary income Dividend income Total income to Calliah Calliah's tax

Sole Proprietorship $55,000 $0 $55,000 $0 $55,000 $37,000 $55,000 $37,000 $0 $7,770 $11,550 $0

C Corporation $55,000 $55,000 $0 $55,000 $37,000 $0 $55,000 $37,000 $0 $0 $0 $18,000 $18,000

S Corporation $55,000 $0 $55,000 $0 $55,000 $37,000 $0 $55,000 $37,000 $0 $0 $0 $18,000 $18,000