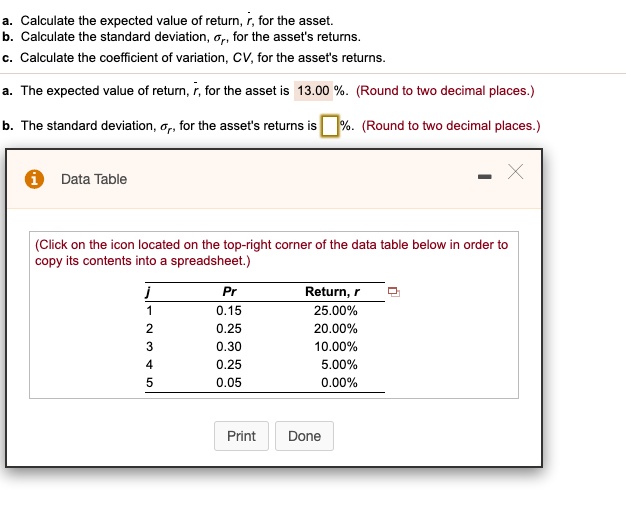

a. Calculate the expected value of return, r, for the asset.

b. Calculate the standard deviation, \(\sigma_r\), for the asset's returns.

c. Calculate the coefficient of variation, CV, for the asset's returns.

a. The expected value of return, r, for the asset is 13.00%. (Round to two decimal places.)

b. The standard deviation, \(\sigma_r\), for the asset's returns is %. (Round to two decimal places.)

Data Table

(Click on the icon located on the top-right corner of the data table below in order to

copy its contents into a spreadsheet.)

j Pr Return, r

1 0.15 25.00%

2 0.25 20.00%

3 0.30 10.00%

4 0.25 5.00%

5 0.05 0.00%

Print Done