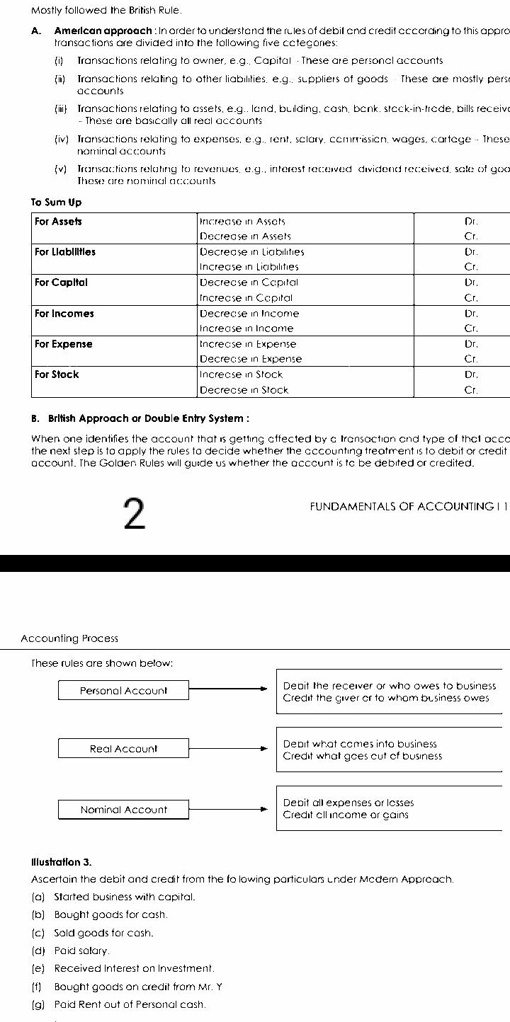

I will vote for your answer definitely according to your work. Most likely followed the British rule. A. American approach: In order to understand the rules of debit and credit according to this approach, transactions are divided into the following five categories:

1. Transactions relating to owners, e.g., Capital - These are personal accounts.

2. Transactions relating to other liabilities, e.g., suppliers of goods - These are mostly personal accounts.

3. Transactions relating to assets, e.g., land, building, cash, bank, stock-in-trade, bills receivable - These are basically all real accounts.

4. Transactions relating to expenses, e.g., rent, salary, commission, wages, carriage - These are nominal accounts.

5. Transactions relating to revenue, e.g., interest received, dividend received, sale of goods - These are nominal accounts.

To Sum Up:

For Assets:

- Increase in Assets: Debit

- Decrease in Assets: Credit

For Liabilities:

- Increase in Liabilities: Credit

- Decrease in Liabilities: Debit

For Capital:

- Increase in Capital: Credit

- Decrease in Capital: Debit

For Incomes:

- Decrease in Income: Debit

- Increase in Income: Credit

For Expenses:

- Increase in Expense: Debit

- Decrease in Expense: Credit

For Stock:

- Increase in Stock: Debit

- Decrease in Stock: Credit

B. British Approach or Double Entry System:

When one identifies the account that is getting affected by a transaction and the type of the transaction, the next step is to apply the rules to decide whether the accounting treatment is to debit or credit the account. The Golden Rules will guide us whether the account is to be debited or credited.