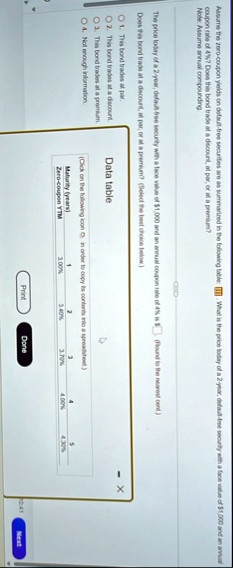

Assume the zero-coupon yields on default-free securities are as summarized in the following table. What is the price today of a 2-year, default-free security with a face value of $1,000 and an annual coupon rate of 4%? Does this bond trade at a discount, at par, or at a premium?

Note: Assume annual compounding.

The price today of a 2-year, default-free security with a face value of $1,000 and an annual coupon rate of 4% is $______. (Round to the nearest cent.)

Does this bond trade at a discount, at par, or at a premium? (Select the best choice below.)

1. This bond trades at par.

2. This bond trades at a discount.

3. This bond trades at a premium.

4. Not enough information.

Data table

(Click on the following icon in order to copy its contents into a spreadsheet.)

Maturity (years)

Zero-coupon YTM

1

3.00%

2

3.40%

3

3.70%

4

4.00%

5

4.30%

Print

Done

Next