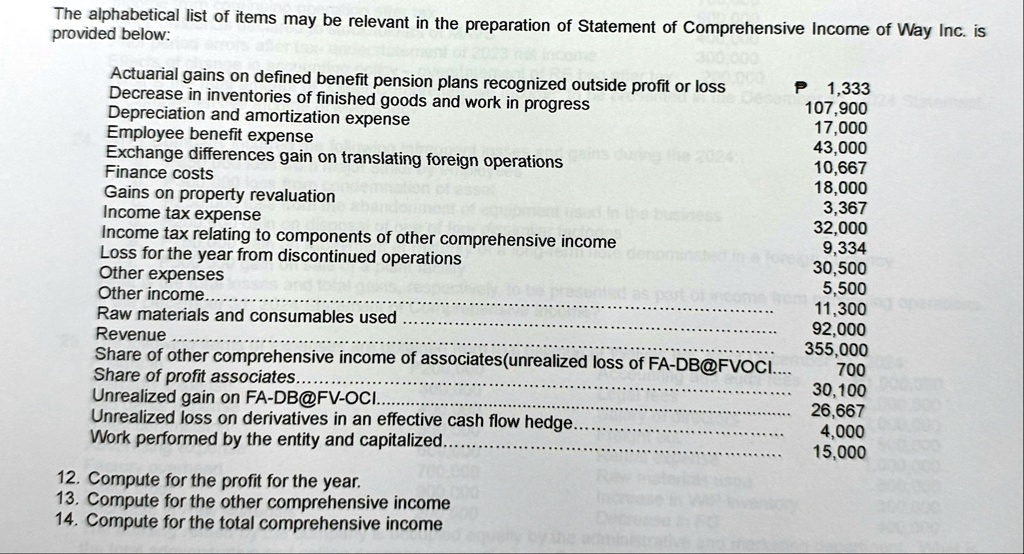

Actuarial gains on defined benefit pension plans recognized outside profit or loss P 1,333

Decrease in inventories of finished goods and work in progress 107,900

Depreciation and amortization expense 17,000

Employee benefit expense 43,000

Exchange differences gain on translating foreign operations 10,667

Finance costs 18,000

Gains on property revaluation 3,367

Income tax expense 32,000

Income tax relating to components of other comprehensive income 9,334

Loss for the year from discontinued operations 30,500

Other expenses 5,500

Other income. 5,500

Raw materials and consumables used 11,300

Revenue 92,000

Share of other comprehensive income of associates(unrealized loss of FA-DB@FVOCI.... 355,000

Share of profit associates... 700

Unrealized gain on FA-DB@FV-OCI.. 30,100

Unrealized loss on derivatives in an effective cash flow hedge. 26,667

Work performed by the entity and capitalized. 4,000

15,000

12. Compute for the profit for the year.

13. Compute for the other comprehensive income

14. Compute for the total comprehensive income