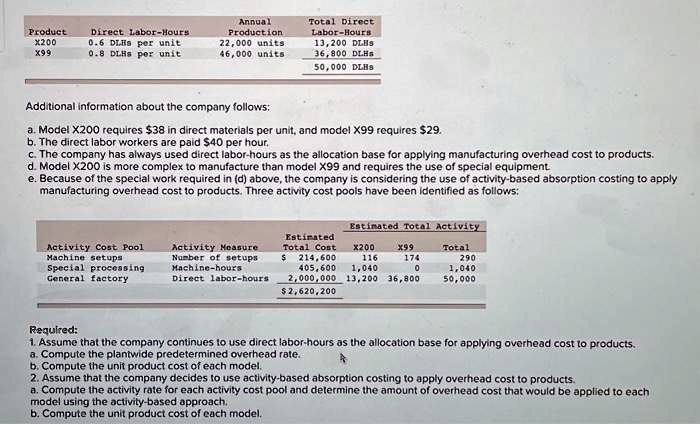

Texts:

Annual Production: 22,000 units, 46,000 units

Total Direct Labor-Hours: 13,200 DLHs, 36,800 DLHs, 50,000 DLHs

Product: X200, X99

Direct Labor-Hours: 0.6 DLHs per unit, 0.8 DLHs per unit

Additional information about the company follows:

a. Model X200 requires $38 in direct materials per unit, and model X99 requires $29.

b. The direct labor workers are paid $40 per hour.

c. The company has always used direct labor-hours as the allocation base for applying manufacturing overhead cost to products.

d. Model X200 is more complex to manufacture than model X99 and requires the use of special equipment.

e. Because of the special work required in (d) above, the company is considering the use of activity-based absorption costing to apply manufacturing overhead cost to products. Three activity cost pools have been identified as follows:

Estimated Total Activity

Estimated Activity Measure Total Cost X200 66% Number of setups 214,600 116 174 Machine-hours 405,600 1,040 0 Direct labor-hours 2,000,000 13,200 36,800 $2,620,200

Activity Cost Pool: Machine setups, Special processing, General factory

Total: 290, 1,040, 50,000

Required:

1. Assume that the company continues to use direct labor-hours as the allocation base for applying overhead cost to products.

a. Compute the plantwide predetermined overhead rate.

b. Compute the unit product cost of each model.

2. Assume that the company decides to use activity-based absorption costing to apply overhead cost to products.

a. Compute the activity rate for each activity cost pool and determine the amount of overhead cost that would be applied to each model using the activity-based approach.

b. Compute the unit product cost of each model.