7-6 Adjust the tax basis in a partnership interest

• 7-7 Apply the basis limitation on the deduction of partnership losses

On January 1, Year 1, Ginger, an individual, paid $16,000 for 5 percent of the stock in Root Corp., an S corporation. In November Year 1,

he loaned $9,000 to Root Corp. in return for a promissory note. Root Corp. generated a $610,000 operating loss in Year 1. Root

Corp. generated $409,000 ordinary business income in Year 2.

Required:

a. How much of Ginger's share of this income is included in his Year 2 taxable income?

b. Compute Ginger's basis in his Root Corp. stock and his Root Corp. note at the end of Year 2.

c. How would your answers to parts a and b change if Root Corp.'s ordinary business income was only $221,000?

Complete this question by entering your answers in the tabs below.

Req A and B

Req C

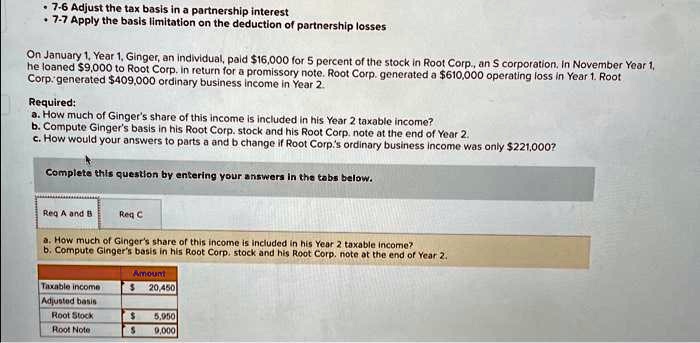

a. How much of Ginger's share of this income is included in his Year 2 taxable income?

b. Compute Ginger's basis in his Root Corp. stock and his Root Corp. note at the end of Year 2.

Amount

Taxable income

$ 20,450

Adjusted basis

Root Stock

$ 5,950

Root Note

$ 9,000