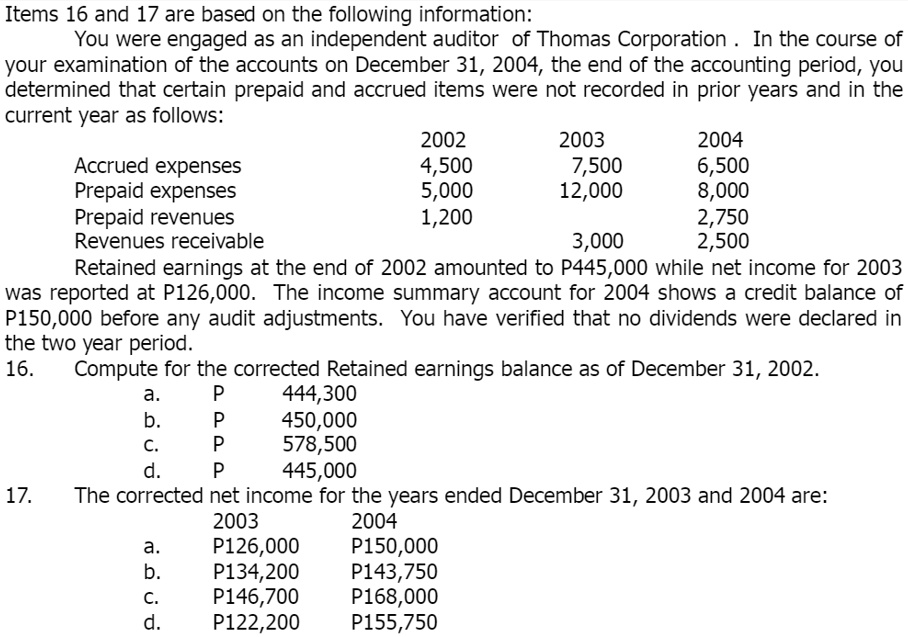

Items 16 and 17 are based on the following information:

You were engaged as an independent auditor of Thomas Corporation. In the course of

your examination of the accounts on December 31, 2004, the end of the accounting period, you

determined that certain prepaid and accrued items were not recorded in prior years and in the

current year as follows:

Accrued expenses

Prepaid expenses

Prepaid revenues

Revenues receivable

2002

2003

2004

4,500

7,500

6,500

5,000

12,000

8,000

1,200

3,000

2,750

2,500

Retained earnings at the end of 2002 amounted to P445,000 while net income for 2003

was reported at P126,000. The income summary account for 2004 shows a credit balance of

P150,000 before any audit adjustments. You have verified that no dividends were declared in

the two year period.

16.

Compute for the corrected Retained earnings balance as of December 31, 2002.

a.

P 444,300

b.

P 450,000

c.

P 578,500

d.

P 445,000

17.

The corrected net income for the years ended December 31, 2003 and 2004 are:

2003

2004

a.

P126,000

P150,000

b.

P134,200

P143,750

c.

P146,700

P168,000

d.

P122,200

P155,750