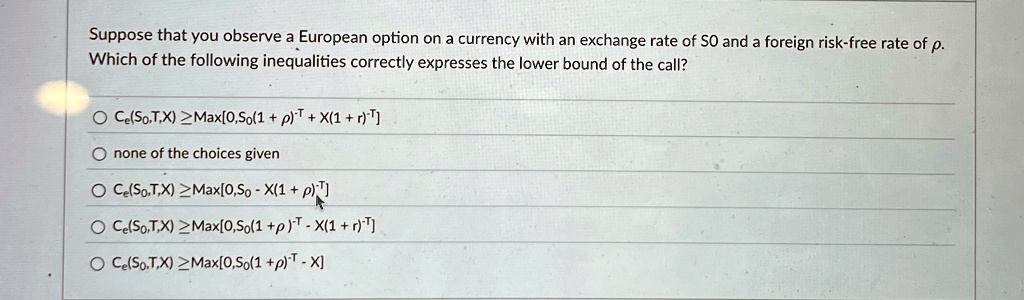

Suppose that you observe a European option on a currency with an exchange rate of $S_0$ and a foreign risk-free rate of $\rho$.

Which of the following inequalities correctly expresses the lower bound of the call?

$C_E(S_0, T, X) \ge \text{Max}[0, S_0(1 + \rho)^T + X(1 + r)^{-T}]$

none of the choices given

$C_E(S_0, T, X) \ge \text{Max}[0, S_0 - X(1 + \rho)^{-T}]$

$C_E(S_0, T, X) \ge \text{Max}[0, S_0(1 + \rho)^{-T} - X(1 + r)^{-T}]$

$C_E(S_0, T, X) \ge \text{Max}[0, S_0(1 + \rho)^{-T} - X]$