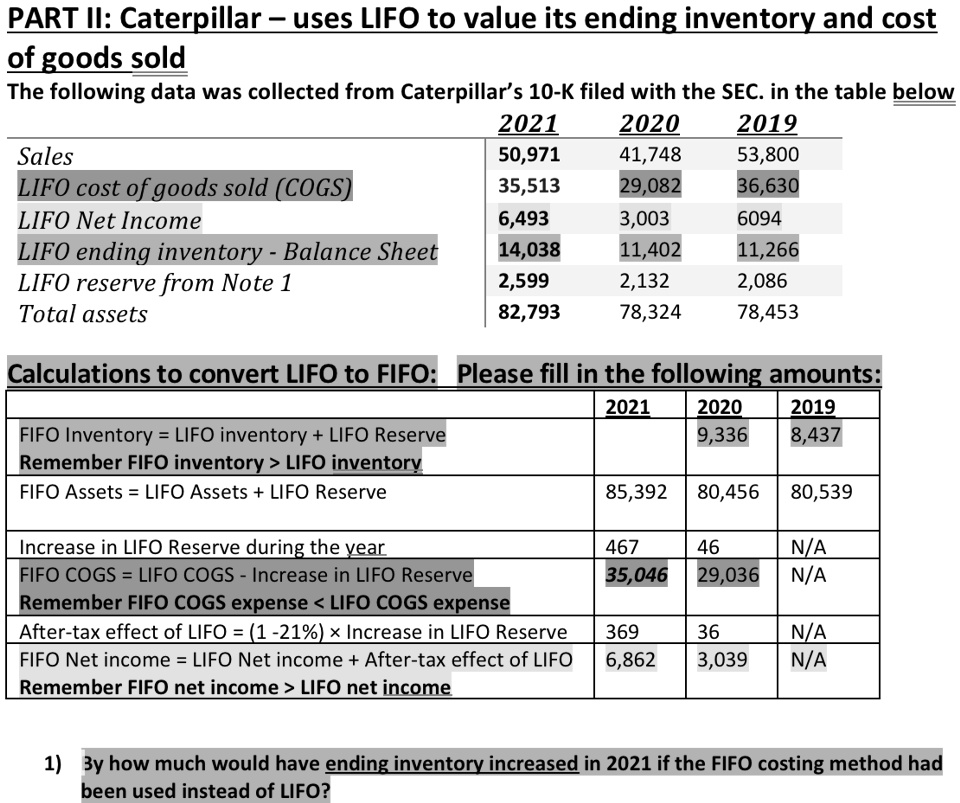

PART II: Caterpillar – uses LIFO to value its ending inventory and cost

of goods sold

The following data was collected from Caterpillar's 10-K filed with the SEC. in the table below

2021

2020

2019

Sales

50,971

41,748

53,800

LIFO cost of goods sold (COGS)

35,513

29,082

36,630

LIFO Net Income

6,493

3,003

6094

LIFO ending inventory - Balance Sheet

14,038

11,402

11,266

LIFO reserve from Note 1

2,599

2,132

2,086

Total assets

82,793

78,324

78,453

Calculations to convert LIFO to FIFO: Please fill in the following amounts:

FIFO Inventory = LIFO inventory + LIFO Reserve

Remember FIFO inventory > LIFO inventory

FIFO Assets = LIFO Assets + LIFO Reserve

Increase in LIFO Reserve during the year

FIFO COGS = LIFO COGS - Increase in LIFO Reserve

Remember FIFO COGS expense < LIFO COGS expense

After-tax effect of LIFO = (1 -21%) × Increase in LIFO Reserve

FIFO Net income = LIFO Net income + After-tax effect of LIFO

Remember FIFO net income > LIFO net income

2021

2020

2019

9,336

8,437

85,392

80,456

80,539

467

46

N/A

35,046

29,036

N/A

369

36

N/A

6,862

3,039

N/A

1) 3y how much would have ending inventory increased in 2021 if the FIFO costing method had

been used instead of LIFO?