Problem 13-10

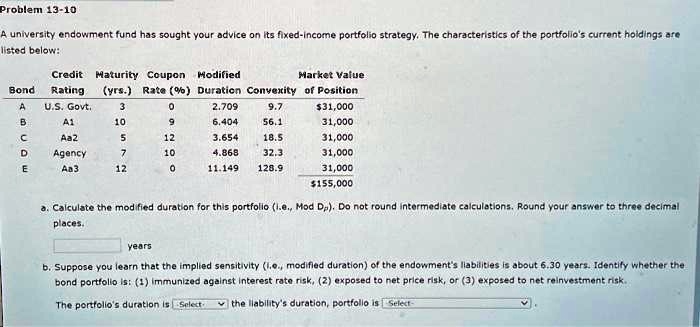

A university endowment fund has sought your advice on its fixed-income portfolio strategy. The characteristics of the portfolio's current holdings are

listed below:

Credit Maturity Coupon Modified

Market Value

Bond

Rating (yrs.) Rate (%) Duration Convexity of Position

A

U.S. Govt.

3

0

2.709

9.7

$31,000

B

A1

10

9

6.404

56.1

31,000

C

Aa2

5

12

3.654

18.5

31,000

D

Agency

7

10

4.868

32.3

31,000

E

Aa3

12

0

11.149

128.9

31,000

$155,000

a. Calculate the modified duration for this portfolio (i.e., Mod Dp). Do not round intermediate calculations. Round your answer to three decimal

places.

years

b. Suppose you learn that the implied sensitivity (i.e., modified duration) of the endowment's liabilities is about 6.30 years. Identify whether the

bond portfolio is: (1) immunized against interest rate risk, (2) exposed to net price risk, or (3) exposed to net reinvestment risk.

The portfolio's duration is Select

the liability's duration, portfolio is Select