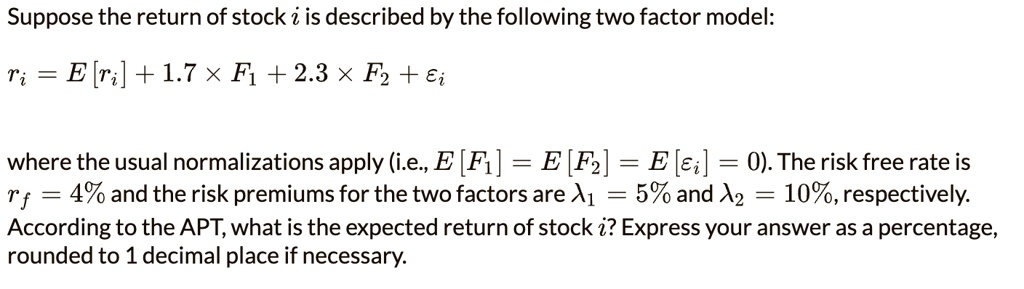

Suppose the return of stock $i$ is described by the following two factor model:

$r_i = E[r_i] + 1.7 \times F_1 + 2.3 \times F_2 + \epsilon_i$

where the usual normalizations apply (i.e., $E[F_1] = E[F_2] = E[\epsilon_i] = 0$). The risk free rate is

$r_f = 4\%$ and the risk premiums for the two factors are $\lambda_1 = 5\%$ and $\lambda_2 = 10\%$, respectively.

According to the APT, what is the expected return of stock $i$? Express your answer as a percentage,

rounded to 1 decimal place if necessary.