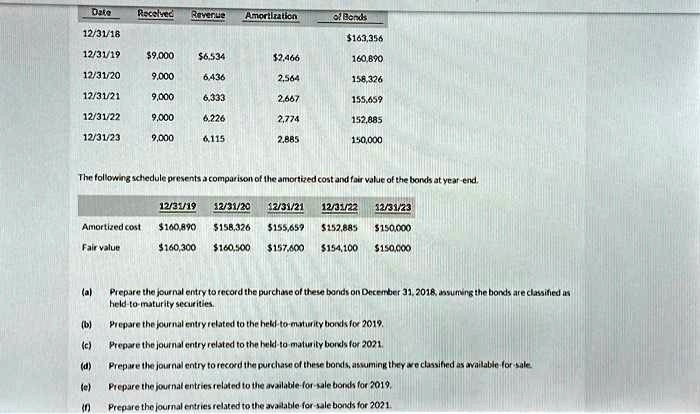

Date

Recelved

Revenue Amortization

of Bands

12/31/18

$163,356

12/31/19 $9,000 $6.534

$2,466

160,890

12/31/20

9,000

6,436

2,564

158,326

12/31/21

9,000

6,333

2,667

155,659

12/31/22

9,000

6.226

2,774

152,885

12/31/23

9,000

6,115

2,885

150,000

The following schedule presents a comparison of the amortized cost and fair value of the bonds at year-end.

12/31/19 12/31/20 12/31/21 12/31/22 12/31/23

Amortized cost $160,890 $158,326 $155,659 5152,885 $150,000

Fair value

$160,300

$160,500 $157,600 $154,100 $150,000

(a) Prepare the journal entry to record the purchase of these bonds on December 31, 2018, assuming the bonds are classified as

held-to-maturity securities.

(b) Prepare the journal entry related to the held-to-maturity bonds for 2019.

(c)

Prepare the journal entry related to the held-to-maturity bonds for 2021.

(d)

Prepare the journal entry to record the purchase of these bonds, assuming they are classified as available-for-sale

(e)

Prepare the journal entries related to the available-for-sale bonds for 2019.

(f)

Prepare the journal entries related to the available-for-sale bonds for 2021.