B. Suppose the marginal cost curve in the short run first decreases, then reaches a minimum, and then increases. If an output is at a point where marginal cost is decreasing, then:

marginal product must be increasing.

average variable cost must be decreasing.

average total cost must be increasing.

marginal product must be increasing and average variable cost must be decreasing.

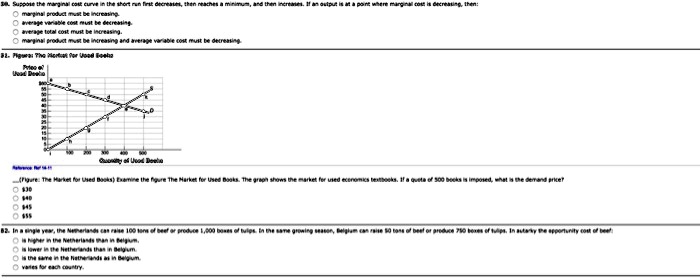

82. Piguras The

Preo

Wood Deeho

(Figure: The Market for Used Books) Examine the figure The Market for Used Books. The graph shows the market for used economics textbooks. If a quota of 500 books is imposed, what is the demand price?

$30

$40

$45

$55

82. In a single year, the Netherlands can raise 100 tons of beef or produce 1,000 boxes of tulips. In the same growing season, Belgium can raise 50 tons of beef or produce 750 boxes of tulips. In autarky the opportunity cost of beef

is higher in the Netherlands than in Belgium.

is lower in the Netherlands than in Belgium.

is the same in the Netherlands as in Belgium.

varies for each country.