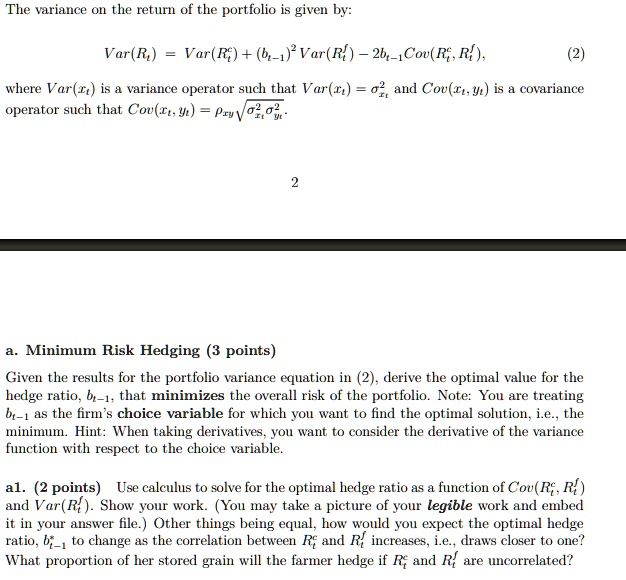

The variance on the return of the portfolio is given by:

$\text{Var}(R_t) = \text{Var}(R_f^t) + (b_{t-1})^2 \text{Var}(R_f^t) - 2b_{t-1} \text{Cov}(R_f^t, R_t^t)$, (2)

where $\text{Var}(x_i)$ is a variance operator such that $\text{Var}(x_i) = \sigma_{x_i}^2$, and $\text{Cov}(x_i, y_i)$ is a covariance

operator such that $\text{Cov}(x_i, y_i) = \rho_{xy} \frac{\sigma_{x_i} \sigma_{y_i}}{}$,

a. Minimum Risk Hedging (3 points)

Given the results for the portfolio variance equation in (2), derive the optimal value for the

hedge ratio, $b_{t-1}$, that minimizes the overall risk of the portfolio. Note: You are treating

$b_{t-1}$ as the firm's choice variable for which you want to find the optimal solution, i.e., the

minimum. Hint: When taking derivatives, you want to consider the derivative of the variance

function with respect to the choice variable.

a1. (2 points) Use calculus to solve for the optimal hedge ratio as a function of $\text{Cov}(R_f^t, R_t^t)$

and $\text{Var}(R_t^t)$. Show your work. (You may take a picture of your legible work and embed

it in your answer file.) Other things being equal, how would you expect the optimal hedge

ratio, $b_{t-1}$ to change as the correlation between $R_f^t$ and $R_t^t$ increases, i.e., draws closer to one?

What proportion of her stored grain will the farmer hedge if $R_f^t$ and $R_t^t$ are uncorrelated?