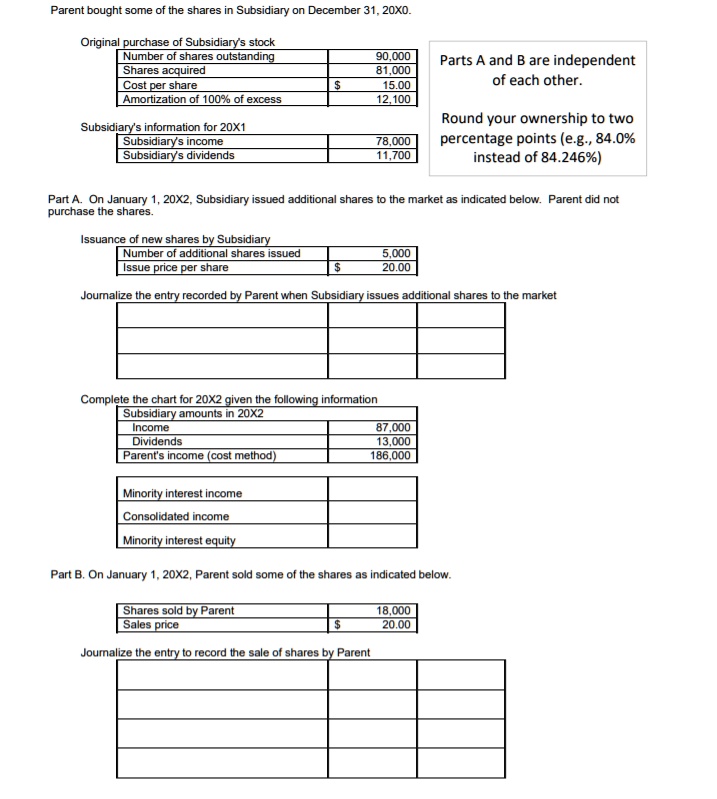

Parent bought some of the shares in Subsidiary on December 31, 20X0.

Original purchase of Subsidiary's stock

Number of shares outstanding

90,000

Shares acquired

81,000

Cost per share

$

15.00

Amortization of 100% of excess

12,100

Subsidiary's information for 20X1

Subsidiary's income

78,000

Subsidiary's dividends

11,700

Parts A and B are independent

of each other.

Round your ownership to two

percentage points (e.g., 84.0%

instead of 84.246%)

Part A. On January 1, 20X2, Subsidiary issued additional shares to the market as indicated below. Parent did not

purchase the shares.

Issuance of new shares by Subsidiary

Number of additional shares issued

5,000

Issue price per share

$

20.00

Journalize the entry recorded by Parent when Subsidiary issues additional shares to the market

Complete the chart for 20X2 given the following information

Subsidiary amounts in 20X2

Income

87,000

Dividends

13,000

Parent's income (cost method)

186,000

Minority interest income

Consolidated income

Minority interest equity

Part B. On January 1, 20X2, Parent sold some of the shares as indicated below.

Shares sold by Parent

18,000

Sales price

$

20.00

Journalize the entry to record the sale of shares by Parent